A call comes in from a hospital far from home. Your spouse, parent, or child is stable for the moment, but the local team says they may need a medical flight to a larger hospital or back to their home state. You're trying to answer three questions at once. Is the transfer medically safe, who arranges it, and who's going to pay for it?

That's where people often stumble with air evac insurance. The name sounds simple, but the actual decision sits at the intersection of medicine, logistics, and insurance rules. A policy might help. A membership might help in some situations. A travel plan might cover evacuation abroad but not a hospital-to-hospital transfer at home. And in the middle of a crisis, families usually don't have time to sort out those differences from a policy booklet.

The practical question isn't just “Do we have coverage?” It's “Will this specific flight, on this date, with this provider, for this medical reason, from this location to this receiving hospital, be covered?”

When a Medical Crisis Happens Far from Home

A common scenario looks like this. A retired couple is spending the winter in another state. One of them has a stroke, a fall, or a cardiac event. The local hospital can stabilize the patient, but the specialists the family trusts are back home. The patient may be too fragile for a long car ride or a standard commercial flight. The family wants the transfer done quickly, safely, and without creating a second emergency in the form of a crushing bill.

That moment is when air evacuation stops being an abstract insurance topic. It becomes a coordination problem with real consequences. Someone has to confirm the patient is stable enough to move, find an accepting facility, match the aircraft and medical crew to the patient's condition, line up ground transport on both ends, and sort out financial responsibility before the aircraft ever lifts off.

The money involved is one reason this topic gets urgent fast. In 2017, the median price for a helicopter air ambulance ride was $36,400 and a fixed-wing air ambulance ride was $40,600, before insurance coverage was considered, according to air ambulance cost statistics summarized by FlyREVA. That same summary notes that patients often faced surprise out-of-network bills averaging nearly $20,000.

Practical rule: If a family is asking about air transport, ask two questions immediately. “Is this medically necessary?” and “Who is the billing provider?”

Families also get tripped up by timing. A transport can be clinically appropriate, but not arranged in a way the insurer accepts. Or it can be approved medically, but still routed through an out-of-network provider. The stress comes from trying to solve all of that while your attention belongs with the patient.

A worried daughter might ask, “Can't we just get Dad home?” Sometimes yes. Sometimes not yet. Sometimes the right answer is a specialized medical escort on a commercial aircraft, and sometimes it's a dedicated air ambulance. Air evac insurance matters because those options aren't interchangeable, and neither are their coverage rules.

What Air Evacuation Insurance Actually Covers

A family often hears, “The flight is covered,” and assumes the financial question is settled. In real transport coordination, that phrase only answers one part of the problem.

Air evac insurance is usually tied to the full medical transport episode. The aircraft matters, but so do the crew, the level of monitoring, the handoff between facilities, and the ground segments on each end. A good way to picture it is a relay race. If one runner drops the baton, the transfer is disrupted. Coverage works in a similar way. One approved flight leg does not guarantee every related service is paid.

The bedside-to-bedside idea

Coverage often follows the patient from the sending bedside to the receiving bedside, not just from airport to airport. Some policies pay for the in-flight medical care and may also include transportation to and from the aircraft. That distinction matters because the patient rarely moves in one clean step.

A complete transfer may include:

- Pickup at the sending facility: A ground ambulance may be needed to take the patient from the hospital to the departure airport.

- The air medical leg: This is the medically equipped aircraft, plus the clinical crew and onboard equipment.

- Arrival coordination: Another ground team may be needed to move the patient from the airport to the receiving hospital.

- Clinical handoff: Records, medications, ventilator settings, and report all have to arrive intact and in sync with the patient.

Families often focus on the plane because it is the visible, dramatic part. Billing does not work that way. Each leg may have a different provider, and each provider may bill separately.

Emergency, urgent, and non-emergency flights

Coverage also changes based on why the patient is flying.

An emergency transport is the scenario people usually picture first. The patient needs rapid access to trauma care, stroke treatment, cardiac intervention, neonatal services, or another higher level of care that is not available locally.

An urgent interfacility transfer is more nuanced. The patient may be stable enough to move, but still needs ICU monitoring, specialty staff, or equipment that the current hospital cannot provide. These flights are common, and they often trigger detailed review of medical necessity, receiving-facility acceptance, and whether a less intensive transport could have done the job safely.

A non-emergency medical flight sits in a different category. The patient may need oxygen, a stretcher, a nurse escort, or close observation without needing a true air ambulance. Many policies draw a firm line here. They may cover transport required for the patient's medical condition, but not a flight chosen mainly for comfort, family convenience, or the desire to return home sooner.

Coverage usually follows the patient's clinical needs and the insurer's medical-necessity rules on that day.

That is why the operational questions matter. Does the patient need a critical care team or a basic medical escort? Is a fixed-wing aircraft required for distance, or would ground transport meet the medical need? Is the receiving hospital formally accepting the patient? Those details affect both safety and payment.

Another common point of confusion is how this fits with Medicare or a regular health plan. If that is part of your decision, this guide on whether Medicare covers air ambulance is a useful starting point.

What coverage is really buying

At its best, air evac coverage does three jobs.

First, it gives access to a medically appropriate level of transport. Second, it sets the payment rules, including which services are eligible and which providers the plan will recognize. Third, it attaches conditions to that payment, such as prior authorization, medical necessity, network status, and documentation from the sending and receiving facilities.

That last piece causes the most confusion. A policy can exist, the flight can occur, and the claim can still be reduced or denied if the transport setup did not match the policy requirements. For families and case managers, the safer approach is to ask two questions before wheels-up: “What level of transport is medically required?” and “Which parts of this transfer are covered, provider by provider?”

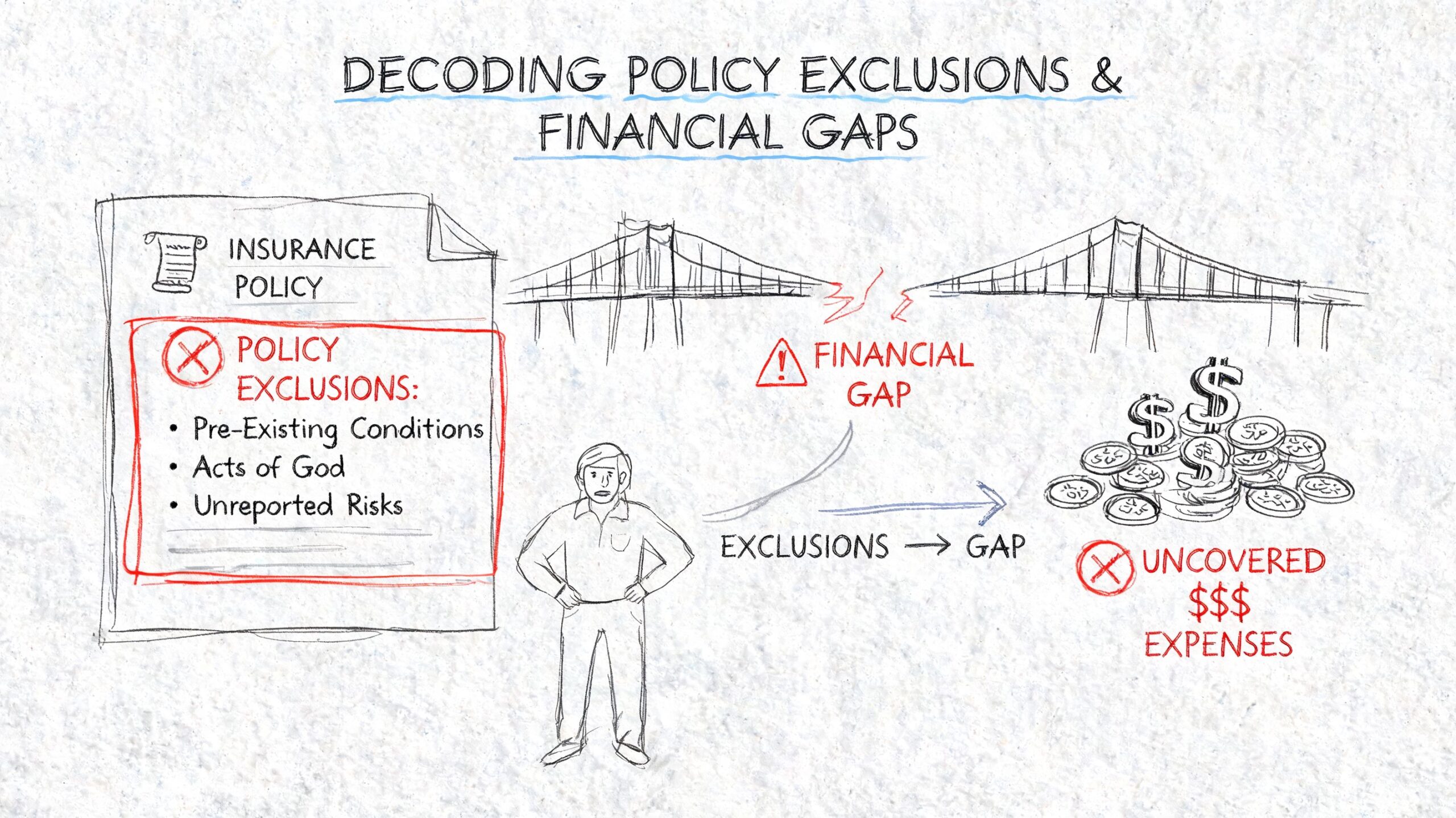

Decoding Policy Exclusions and Financial Gaps

Families and case managers need to slow down and read carefully at this point. The most expensive mistake isn't failing to buy a policy. It's assuming a policy pays the whole bill in every medically stressful situation.

The billed amount and the allowed amount

One of the biggest hidden gaps is the difference between the provider's billed amount and the insurer's allowed amount. Industry FAQs from AirMedCare Network's air ambulance FAQ page note that many insurers may reimburse 100% of the allowed amount for air ambulance or emergent ground transport. That sounds reassuring until you realize the provider may charge more than the insurer allows.

If that happens, the patient may still owe:

- A deductible

- Coinsurance or copays

- Any balance above the insurer's allowed amount, depending on the claim and applicable billing protections

That's why “covered” and “paid in full” are not the same thing.

The network problem

Network status has historically been one of the biggest financial hazards in this space. A large U.S. claims study covering 36,312 air ambulance claims over four years found that 77% of all claims were out-of-network, including 24,965 of 32,215 rotary-wing claims and 2,884 of 4,097 fixed-wing claims, according to the peer-reviewed claims study on air ambulance networks.

For families, that means this: you can have health insurance and still end up in a transport that your insurer treats as outside its contracted provider system.

What this means in practice: Before launch, ask whether the air ambulance company is in-network for the patient's plan, or whether payment will be based on the insurer's own allowance schedule.

If you're comparing quotes or trying to understand why one transport is priced differently from another, this breakdown of what impacts air ambulance cost and what you'll be asked when you call helps frame the right operational questions.

Exclusions that catch people off guard

Some exclusions are obvious only after a claim is denied. Others are tucked into definitions and transport criteria. Watch for these categories:

- Medical necessity rules: The insurer may decide the patient could have gone by ground or by another transport mode.

- Geographic limits: A plan may limit coverage based on distance, nearest appropriate facility, or airport access criteria.

- Aircraft restrictions: Some policies distinguish between helicopter and fixed-wing transport.

- Companion limits: A family member's seat may not be covered unless the plan says so.

- Bedside scope limits: If the policy doesn't clearly include both ground legs, families may end up paying separately.

Questions worth asking before anyone signs

A short checklist can prevent a very long billing dispute:

| Question | Why it matters |

|---|---|

| Is this provider in-network for the patient's plan? | Network status can affect patient balance responsibility. |

| Will the insurer pay billed charges or only an allowed amount? | This identifies possible balance billing risk. |

| Does the policy cover both ground legs and the air leg? | “Bedside-to-bedside” isn't automatic in every plan. |

| Does the insurer require prior authorization when the transfer is not immediate field emergency transport? | Missing authorization can trigger denial. |

| Is the destination the nearest appropriate facility, or a family-preferred facility? | Coverage may depend on that distinction. |

Families often focus on the aircraft because it feels tangible. Financially, the policy language usually matters more.

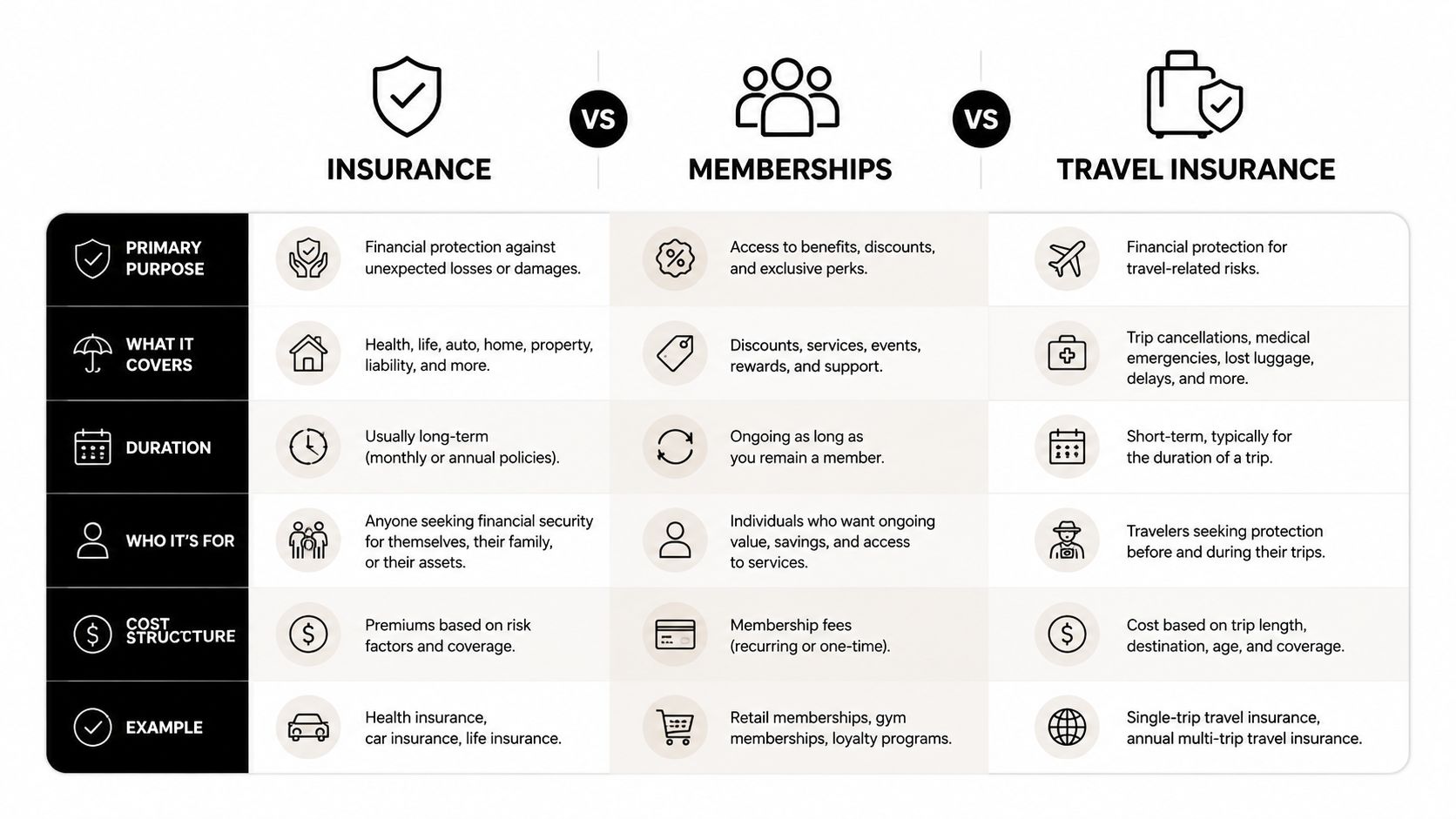

Insurance vs Memberships vs Travel Insurance

Many people use these terms as if they mean the same thing. They don't. That confusion leads to bad assumptions, especially when someone says, “We bought the membership, so we're covered.”

Three products with three different triggers

Air evac insurance is usually tied to covered medical transport under policy terms. The claim lives inside an insurance framework. Medical necessity, network rules, and benefit language drive the outcome.

Air ambulance memberships are not insurance. That distinction matters. As NerdWallet's medical evacuation insurance guide explains, membership plans may not protect you if a different company performs the transport, and government data cited there showed about two-thirds of medical flights for privately insured people were out-of-network in 2017.

Standard travel insurance with medevac benefits often focuses on travel-related evacuation needs, especially when you're away from home or abroad. It can be valuable, but it may not function like a domestic hospital transfer benefit.

Air Evac Coverage Options Compared

| Feature | Air Evac Insurance | Air Ambulance Membership | Standard Travel Insurance (with Medevac) |

|---|---|---|---|

| Coverage trigger | Usually medical necessity and policy terms | Usually transport by participating provider under membership rules | Usually a covered travel event under the policy |

| Provider flexibility | Depends on insurer network and authorization | Often tied to participating fleet or company | Depends on the policy and assistance arrangement |

| Main financial risk | Allowed amount limits, cost sharing, denial | Non-participating aircraft or non-covered scenario | Exclusions, trip conditions, and policy limits |

| Common strength | Can integrate with health coverage | Can reduce out-of-pocket risk within the membership system | Useful for travel-related evacuation support |

| Common misunderstanding | “Covered” means “no bill” | “Membership” means insurance | “Medevac” means any transfer anywhere |

Questions people ask all the time

“Is a membership enough?”

Sometimes it helps a lot. Sometimes it doesn't apply. If the patient is transported by a non-participating company, the membership may not solve the bill.

“Is travel insurance the same as air evac insurance?”

No. Travel policies may be built around trip disruption and emergency evacuation, not every domestic interfacility transfer.

“Where do membership plans fit, then?”

They fit as one tool, not the whole plan. If you want to compare how these programs work, this overview of medical flight memberships is a useful reference point.

A smart setup often layers protection. People use health insurance, then assess whether a membership or travel medevac product fills a gap that their main policy leaves open.

The right choice depends on how you travel, where you spend time, and whether your main concern is emergency scene transport, hospital-to-hospital transfer, or getting back closer to home once stable.

How to Determine If You Need Air Evac Coverage

Not everyone needs the same kind of protection. The useful question isn't “Should everyone buy air evac insurance?” It's “What kind of transfer risk do you face?”

People who should think about it carefully

A snowbird often spends months in another state. That creates a real possibility of needing care far from their home doctors, family support, and preferred rehab network. If you fit that profile, review not just emergency coverage, but whether a plan addresses interfacility transfer and distance-related restrictions.

A business traveler going overseas has a different risk. The concern may be getting out of a remote or unfamiliar medical system and into a facility with language support, known standards, or a route home once stable enough to move.

A family caring for a child with complex medical needs should think in more operational terms. Does the child need specialty monitoring, respiratory support, extra equipment, or a receiving team that must be confirmed before movement? Coverage matters, but so does whether the transport mode fits the child's clinical needs.

An active traveler who skis, dives, hunts, boats, or visits rural destinations should check exclusions and transport criteria. The issue may not be the activity itself. The issue is whether a remote location or unusual transfer path creates a gap between what's medically needed and what the plan will approve.

A simple self-assessment

Ask yourself these questions:

- Where am I most likely to need care? Another state, another country, or a rural area changes the transport equation.

- Would I want transfer to the nearest appropriate hospital, or back closer to home? Those aren't always covered the same way.

- Do I already have a condition that increases transfer risk? Cardiac, neurologic, respiratory, and bariatric needs often affect transport planning.

- Who would coordinate this if I were unable to speak for myself? A spouse or adult child should know where policy documents are.

- What's my real financial tolerance? Some families can absorb deductibles and disputes. Others want more predictable protection.

When coverage tends to matter most

Air evac coverage deserves a harder look if you have any combination of:

- Frequent travel away from your home medical team

- A medically fragile family member

- A strong preference for transfer to a specialized center

- Concern about remote, rural, or cross-state transport

- Limited ability to absorb a large unexpected bill

For some people, the answer will be yes. For others, the better move is to improve organization first. Keep insurance cards current, list your medications, store emergency contacts, and make sure your health care proxy knows your wishes.

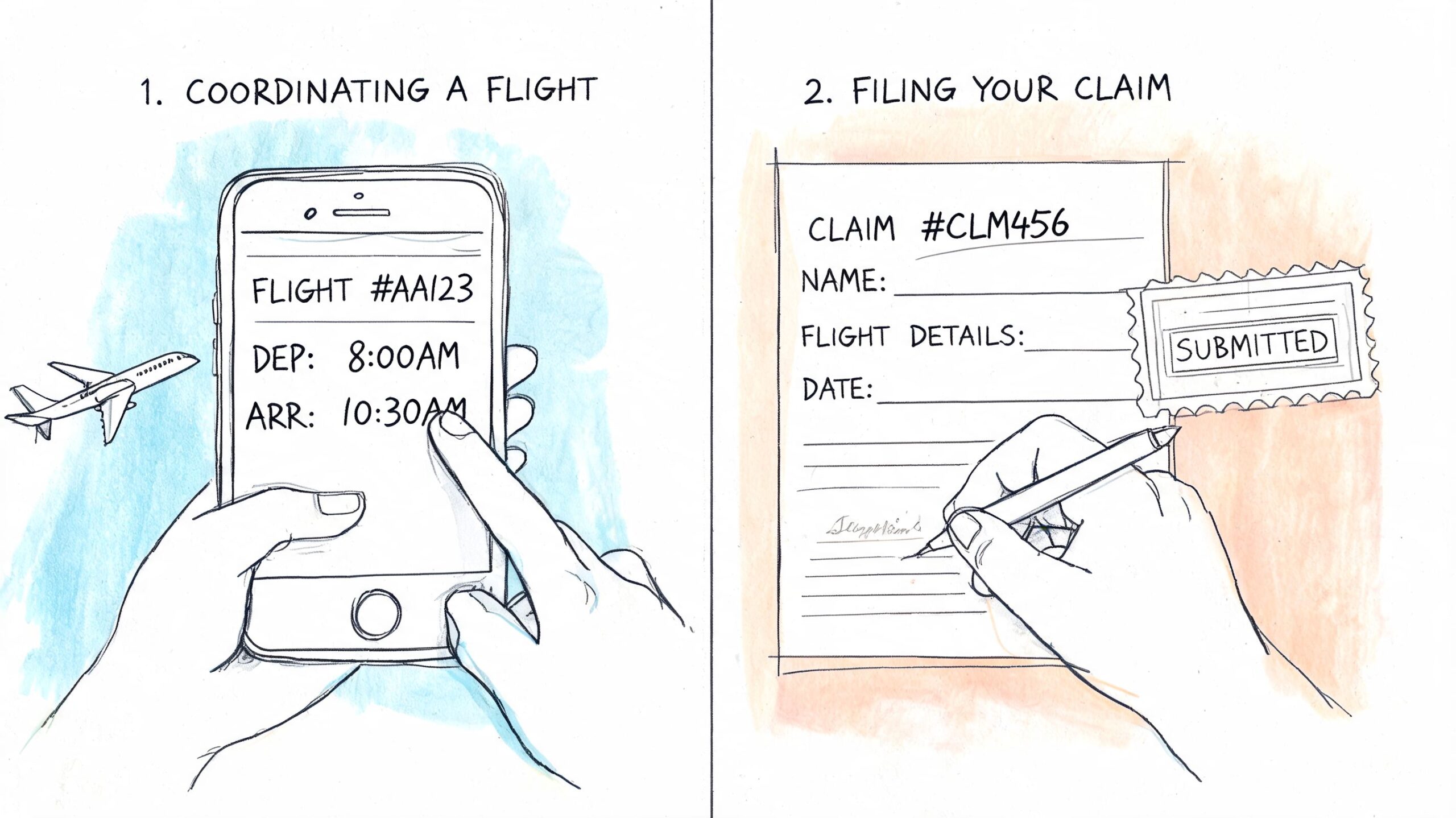

Coordinating a Flight and Filing Your Claim

At 2 a.m., the bedside doctor says your family member needs a medical flight. In that moment, the aircraft is only one part of the job. Someone also has to confirm the receiving hospital, match the crew to the patient's condition, clarify who is authorizing the trip, and preserve the paperwork that will decide whether the claim is paid or disputed later.

What to do first

Start with the treating team, not the aircraft dispatcher. The first question is whether the patient can safely move at all. The next question is what kind of transport team is required during the trip. A stable patient going to a regional hospital is a different operation from a ventilated patient going to a specialty center across state lines.

Then contact the insurer, assistance company, or whoever handles authorization under the policy. Ask them to explain the trigger for coverage in plain language. For example, are they approving transfer to the nearest appropriate hospital, or will they also consider a transfer to a preferred facility closer to home? Are both air and ground legs part of the same approval, or do they need separate authorization? Those details are where coverage gaps often start.

A medical flight works like a relay handoff. If one runner misses the exchange, the whole transfer slows down.

Information you should have ready

The person making calls should gather the details that operations, clinical staff, and billing all need at the same time:

- Patient details: full name, date of birth, diagnosis, current location

- Clinical status: oxygen needs, monitoring needs, isolation issues, mobility limits

- Hospital contacts: sending physician, case manager, bedside nurse, receiving facility contact

- Insurance details: plan name, member ID, authorization contact

- Documents: face sheet, medication list, recent notes, imaging status, physician orders when available

If there's an accident involved and you expect contact with insurers beyond the health plan, families sometimes benefit from a plain-language guide for accident victims that explains how to handle insurance adjuster conversations without saying too much too early.

Questions to ask the air ambulance provider

The transport company is not just selling a seat on an airplane. It is taking responsibility for a moving ICU, a handoff between facilities, and often two separate ground transfers. That is why practical questions matter as much as the policy language.

Ask questions like these:

- Are you the direct aircraft operator or are you arranging this through another company?

- What clinical crew will be on board for this patient's condition?

- Can your team manage the patient's oxygen, ventilator, cardiac, bariatric, or isolation needs?

- Do you arrange both ground legs, or only the flight itself?

- Who is confirming acceptance with the receiving hospital and bed availability?

- What records must be sent before departure so the crew can launch without delay?

- Will you bill insurance directly, and how do you handle flights that leave before final authorization is issued?

Clear answers help you spot two common problems early. One is assuming the flight provider is coordinating the full transfer when they are only arranging the aircraft. The other is assuming the ordered crew level matches the patient, even though equipment or medication needs may require a different team.

One option families and case managers may encounter is Med Jets by Air Trek, which coordinates fixed-wing medical transport along with ground transport and hospital-to-hospital logistics. Whether you use that program or another provider, the same operational questions still apply.

Filing the claim without losing key details

Once the flight is complete, treat the claim file like a chain of custody. You want a clear record of why the transfer happened, who approved it, what level of care was provided in transit, and what each party agreed to bill.

Save the authorization record, transport agreement, physician certification if one was used, hospital records, itemized billing, and all insurer correspondence. If the provider obtained verbal approval, ask for the reference number and the name of the representative who gave it.

A short habit helps more than people expect. After every phone call, write down:

- Who you spoke with

- The date and time

- What they approved or stated

- Any reference or authorization number

Those notes can protect you if the claim is later questioned over medical necessity, network status, denied ground segments, or services provided during the flight that were never discussed at dispatch.

Essential Checklists for Families and Case Managers

Family checklist

- Gather insurance documents: Bring the health plan card, membership details if any, and photo ID.

- Confirm the destination: Ask why this hospital was chosen and whether it is the nearest appropriate facility or a family-preferred transfer.

- Ask about companions: Find out whether a family member can fly and whether that seat is covered.

- Pack for transfer day: Include glasses, hearing aids, chargers, medication list, legal documents, and a small bag for the receiving hospital.

- Write down names: Keep the names of the sending nurse, physician, dispatcher, and receiving contact.

Hospital case manager checklist

- Confirm acceptance: Make sure the receiving physician and bed are secured before launch.

- Assemble the handoff packet: Face sheet, MAR, physician orders, recent clinical notes, imaging status, and nurse report.

- Match the transport to the patient: Verify aircraft type, crew level, oxygen requirements, isolation needs, and bariatric or equipment needs.

- Clarify payer status: Document authorization steps, insurer contacts, and any unresolved network questions.

- Close the loop: Confirm ETA updates are going to the sending unit, receiving unit, and family contact.

Air evac insurance works best when it's paired with disciplined coordination. In a medical flight, the safest financial decision and the safest clinical decision are often the same one. Ask specific questions early, document everything, and never assume that “covered” means every part of the transfer is handled.