When that call comes, nobody starts by thinking about billing codes or network rules. A spouse is in another state after a stroke. A parent is stable enough to move but not safe to ride for hours by ground. A hospital case manager says a transfer may be needed today, and the family's first practical question lands hard.

Does insurance cover air ambulance?

Sometimes yes. Sometimes partially. Sometimes only after a fight over medical necessity, destination, or paperwork. In real cases, coverage often depends less on the word “emergency” and more on whether the chart, physician order, and transport plan clearly show why a flight was the right level of care.

Families usually need answers fast. They also need someone to slow the process down just enough to avoid expensive mistakes. The most useful approach is to treat the transport as both a clinical transfer and an insurance event. If either side is handled poorly, the flight can still happen, but the financial outcome gets harder to control.

The Urgent Call and the First Big Question

A common situation looks like this. Your loved one is hospitalized away from home. The local team has stabilized the immediate crisis, but they want the patient moved to a hospital with different specialists, a higher level of monitoring, or a location closer to long-term support. You hear terms like ICU bed, bedside report, accepting physician, and transport window. Then someone asks whether the family wants to proceed.

That's the moment when panic and paperwork collide.

Families often assume one of two things, and both can be risky. The first is, “If a doctor says they need a plane, insurance will pay.” The second is, “If it's expensive, there's no point even trying.” Neither is reliable. Insurance may cover a medically necessary flight, but approval usually depends on how the need is documented, which provider performs the transport, and whether the transfer is to the nearest appropriate facility.

Practical rule: Before anyone focuses on aircraft type or scheduling, confirm three things. Why the patient can't go safely by ground, why the receiving hospital is appropriate, and who is talking to the insurer.

That early coordination matters more than is often appreciated. A rushed transfer with weak documentation can trigger denials later. A carefully coordinated one gives the insurer a clearer basis to approve, and it gives the family fewer billing surprises to sort out after the crisis.

If you're trying to understand what happens from first call through bedside transfer, this overview of emergency medical transport services gives a useful picture of how the process is typically coordinated.

Understanding Medical Necessity for Air Ambulance

Insurance decisions usually turn on one phrase: medical necessity. That phrase sounds abstract, but in practice it's very concrete. The insurer wants to know why this patient needed an air ambulance instead of another transport option.

What insurers usually look for

Consider a physician choosing a higher-acuity treatment. If an over-the-counter option would reasonably work, the stronger intervention is harder to justify. Air ambulance works the same way. The file has to show why ground transport was not appropriate and why the patient needed in-flight medical care or faster access to the next facility.

The strongest approvals usually rest on a combination of factors such as:

- Ground transport isn't clinically safe: The patient may need monitoring, ventilator support, medication management, or a shorter travel time than ground can provide.

- The receiving hospital offers necessary care: The transfer should connect clearly to treatment the sending hospital can't provide.

- The transport itself requires a medical team: If the patient needs skilled care in transit, that supports the need for air transport rather than routine travel.

- The record is consistent: The physician order, nursing notes, case management notes, and transfer request should all tell the same story.

What documentation actually helps

In day-to-day coordination, weak documentation is one of the biggest reasons claims become difficult. “Patient prefers to be closer to home” may be emotionally compelling, but it usually won't carry an insurance claim by itself. “Patient requires transfer for specialty care unavailable at current facility, and prolonged ground time is not appropriate” is much stronger when backed by chart notes.

A usable file often includes:

- Physician certification or order explaining why air transport was needed.

- Hospital records showing the current condition, recent treatment, and transfer rationale.

- Receiving facility acceptance from the physician or unit taking the patient.

- Transport clinical notes describing what care was required during the flight.

The chart has to answer the insurer's question before the insurer asks it.

Questions families should ask early

Families don't need to speak insurance language perfectly. They do need to ask the right practical questions.

- Can you document why ground isn't appropriate?

- Is the receiving hospital the nearest appropriate facility for this level of care?

- Who is obtaining the medical records and physician statement for the claim?

- Has anyone checked whether preauthorization is required if the patient is stable enough for planned transfer?

When people ask “does insurance cover air ambulance,” the actual answer is often, “It depends on how convincingly medical necessity is established.”

How Different Insurers Handle Air Ambulance Claims

Different payers look at the same flight through different rules. That's why two families can face very different outcomes even when the medical situation looks similar.

One of the clearest gaps appears in payment levels. From 2017 to 2020, the estimated allowed amounts for fixed-wing air ambulance services under private insurance rose 76.4%, from $8,855 to $15,624, while Medicare reimbursements grew 4.7%, from $3,071 to $3,216 according to a National Library of Medicine collection document. That gap helps explain why families are often surprised by what a plan approves versus what a provider bills.

Air Ambulance Coverage by Insurance Type

| Insurance Type | Medical Necessity Standard | Typical Coverage | Common Pitfall |

|---|---|---|---|

| Private PPO | Usually requires proof that air was medically necessary and ground was not appropriate | May cover a significant portion if criteria are met, but payment may be limited to what the plan considers reasonable | Out-of-network disputes and partial payment |

| Private HMO | Often stricter about authorization and network coordination | Can be limited if the transfer is outside the plan's referral path | No prior approval, non-network receiving facility |

| Medicare | Covers only under specific medical necessity rules, generally when other transport is inappropriate | Payment is based on Medicare's reimbursement structure, not provider charge | Transfer not meeting Medicare criteria or not to the nearest appropriate facility |

| Medicaid | Rules vary by state and program administration | May cover medically necessary flights with strong documentation | State-specific approval requirements and administrative delays |

| Travel insurance | Depends heavily on policy language and whether transport assistance is included | Can be useful for cross-border or travel-related events if purchased in advance | Policy exclusions and repatriation limitations |

Private insurance

Commercial plans often do cover air ambulance, but the approval path is narrow. The insurer may agree that a flight was medically necessary, then still argue over the amount payable. That's where families hear phrases like “usual and customary” or “reasonable reimbursement.”

Private plans also tend to separate the clinical question from the network question. A patient can win the first argument and still lose part of the second.

If you're comparing senior coverage rules specifically, this guide on whether Medicare covers air ambulance is a useful companion to the broader insurance picture.

Medicare and Medicaid

Medicare tends to be more formula-driven. If the transfer doesn't fit the program's standard for medical necessity, the claim can fail even when the family felt there was no realistic alternative. Medicare also generally focuses on transport to the nearest appropriate facility, which becomes important when a family hopes to move someone closer to home.

Medicaid can cover medically necessary air transport, but the practical experience varies by state and managed care arrangement. In some cases, the medicine supports the flight clearly, but the administrative steps still slow everything down.

Travel insurance and secondary coverage

Travel insurance matters most when standard health coverage gets thin, especially across state lines or international borders. It can also matter when the issue is not just hospital-to-hospital transfer, but bedside-to-bedside coordination, escort support, or return travel after stabilization.

A family's best payer on paper isn't always the payer that moves fastest. The plan with cleaner authorization rules often creates less stress than the plan with broader language but more disputes.

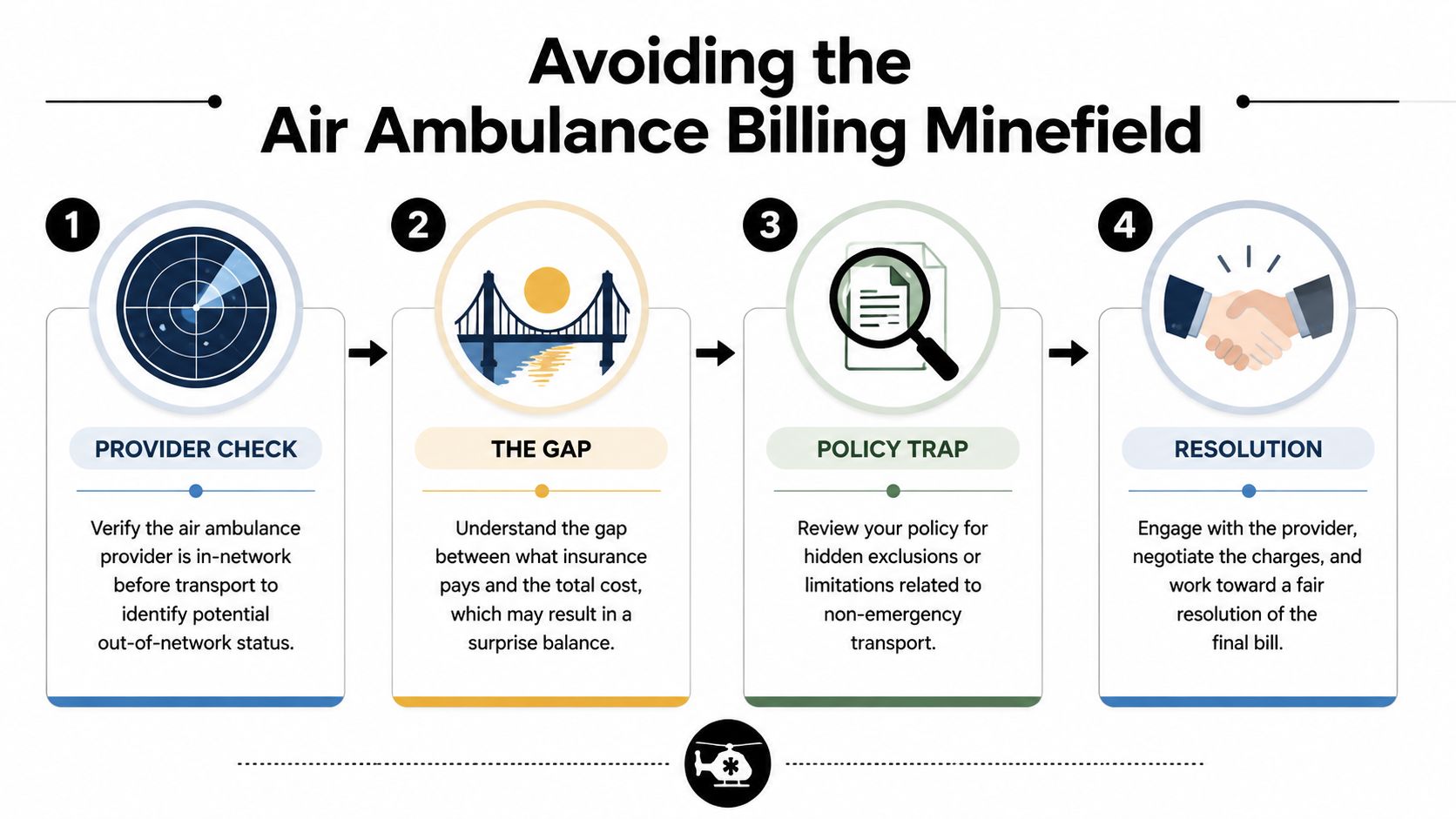

Navigating Common Exclusions and Billing Pitfalls

Air ambulance billing problems usually come from a small set of recurring issues. The flight happens quickly, but the claim is reviewed slowly. By the time the bill arrives, the family is no longer dealing with the emergency. They're dealing with coverage language.

The exclusions that cause the most trouble

Some denials are based on the core question of necessity. Others turn on details that didn't seem important in the moment.

Common trouble spots include:

- Out-of-network status: The insurer may acknowledge the flight but dispute the amount.

- Destination choice: If the transfer wasn't to the nearest appropriate facility, the plan may limit payment.

- Non-emergency interpretation: A stable patient transfer can still be medically necessary, but the record has to prove why air transport was required.

- Insufficient documentation: Missing physician statements, incomplete records, or vague transfer notes weaken the file.

For families trying to understand plan terms before a claim issue develops, it can help to review examples of individual policy structures such as ISU Insurance Services Aetna plans, then compare that language against the patient's actual benefits.

What the No Surprises Act does and doesn't do

The No Surprises Act gave many families the impression that air ambulance bills had been solved. It helped, but it didn't remove the underlying claim fights. A 2024 Government Accountability Office report highlighted that air ambulance billing disputes rose 15% after the law took effect, with patients still facing average balance bills of $25,000 to $50,000 when insurers and providers disagree on reasonable payment, as described in this air ambulance insurance discussion.

The important distinction is this: a law can limit some surprise billing exposure without guaranteeing that the insurer will approve the claim in the first place.

How to reduce the damage before the bill arrives

Families can't control every part of an emergency transfer, but they can reduce risk.

- Ask who is in network: If the situation allows any choice, verify the transport provider's insurance relationships.

- Confirm the receiving facility rationale: The chart should show why that hospital was appropriate.

- Request copies early: Keep the physician order, acceptance note, and transport records before memories and staff availability change.

- Understand the cost drivers: This overview of what impacts air ambulance pricing and what callers are asked helps families understand where billing questions usually start.

Billing disputes are easier to prevent than to unwind. Once a claim is framed the wrong way, every appeal becomes more work.

Your Guide to Preauthorization and Appealing Denials

When a transfer is planned rather than field-emergent, preauthorization can make the difference between a manageable claim and a messy one. That doesn't mean approval is guaranteed. It means the insurer has a chance to review the case before the aircraft is in the air.

According to the Workers Compensation Research Institute, average payments for air ambulance transports in the workers' compensation system surged more than 60% over the past decade, rising from roughly $15,000 in 2013 to 2015 to more than $25,000 in 2022 to 2024, which shows why authorization and documentation matter so much before transport is arranged, as reported by Risk & Insurance covering WCRI data.

Before the flight

Start with the insurer, but don't call empty-handed. Have the patient's ID information, the sending hospital, the receiving hospital, the treating diagnosis, and the physician's transfer rationale ready.

Ask direct questions:

- Is preauthorization required for fixed-wing or helicopter transport in this case?

- What documents must be submitted before review?

- Does the plan require transfer to the nearest appropriate facility?

- Are there network restrictions for the air ambulance provider or receiving hospital?

- If approved, what exactly is being approved: medical necessity, amount, or both?

Build the file like an appeal may be needed later

Many families and even busy hospital teams often lose ground at this point. They submit enough to request the flight, but not enough to defend the claim later.

A stronger packet includes:

- Physician statement: Why air transport was necessary and why ground was not suitable.

- Clinical records: Current condition, treatment provided, and risks of delay.

- Receiving acceptance: Name of accepting physician or facility confirmation.

- Transport plan: Level of onboard care expected during flight.

- Insurance notes: Reference numbers, names of representatives, and dates of calls.

A short educational video can also help families understand the flow of approvals and transfers before they get on the phone with a payer.

If the claim is denied

Don't start with outrage. Start with the denial reason. The appeal has to answer that specific problem.

Use this sequence:

- Read the denial carefully: Lack of medical necessity, out-of-network status, missing documents, and destination issues require different responses.

- Request the full claim file: Ask for the records and notes the insurer relied on.

- Get a more detailed physician letter: It should respond directly to the denial language.

- Submit a timed appeal: Follow the plan's deadlines exactly.

- Escalate if needed: Ask about peer-to-peer review, external review, or state-regulated complaint options where available.

For a broader consumer-facing overview of recurring denial themes, this roundup of top reasons for insurance claim denials can help families frame the issue before drafting an appeal.

How Med Jets by Air Trek Streamlines the Entire Process

The families who struggle most are often handling three separate conversations at once. One with the hospital. One with the insurer. One with the transport provider. Those conversations rarely line up neatly unless one coordinator is pulling them together.

That's where a dedicated transfer coordinator changes the outcome. Instead of leaving the family to collect records, confirm bed acceptance, clarify aircraft capability, and chase authorizations, one point of contact can organize the sequence. The sending hospital provides the clinical picture. The receiving hospital confirms acceptance. The insurer gets the documentation needed to evaluate the request. The transport team builds a plan around the patient's condition and timing.

What that liaison role looks like in practice

In a well-run transfer, the coordinator does more than schedule wheels-up time.

- Hospital coordination: confirming bedside readiness, report timing, and acceptance details

- Documentation support: gathering physician statements, records, and insurance information

- Utilization communication: speaking with payer representatives about medical necessity and authorization steps

- Logistics management: aligning ground transport, airport access, family communication, and arrival handoff

This is also where edge cases matter. Bariatric transport, international planning, and flights involving a family companion often require details that can derail approval if nobody addresses them early.

One option families and case managers use is Med Jets by Air Trek, which works as that liaison between hospitals, family, and insurer while coordinating the transport itself. In practical terms, that can include collecting clinical records, helping present the case for coverage, and working toward a single-case agreement when the claim structure allows it.

The smoother flight is often the one that looked most organized on paper before departure.

If a claim has already been underpaid or mishandled, families may also need outside help understanding their rights. This guide on how to fight a low-balled insurance claim is a useful general reference for the negotiation side of the problem.

Frequently Asked Questions About Air Ambulance Insurance

Does insurance cover air ambulance if the patient is stable?

Sometimes, yes. Stability does not automatically mean a flight is non-covered. The question is whether the patient still required air transport for medical reasons, such as level of onboard care, transfer urgency, or inability to tolerate ground transport safely. Stable transfers are often reviewed more closely, so documentation matters even more.

What if I need an air ambulance while traveling internationally?

This is one of the hardest coverage situations. A 2025 FAIR Health study found that 60% of claims for international air ambulance repatriation are denied by standard health plans, often because the patient is considered no longer in need of medically necessary transport once stabilized abroad, leaving average out-of-pocket costs exceeding $150,000, according to this report on insurance coverage for air ambulance services.

If the patient is outside the U.S., ask two questions immediately: does the health plan cover international medical transport, and is there travel insurance or assistance coverage that can coordinate repatriation?

Will insurance pay to move someone closer to home?

Sometimes, but families often run into disappointment. A move closer to home can make emotional and practical sense without meeting the plan's standard for medical necessity. If the clinical record shows the patient needs a different level of care at the receiving facility, coverage is more likely than if the reason is convenience or family proximity alone.

Should I buy a separate air ambulance membership?

It depends on your travel habits, health status, and where you live. Memberships and transport assistance products can be useful when standard insurance leaves large gaps, especially for rural access or travel-related events. They are not all structured the same, so read the service area, provider limitations, and claim coordination terms carefully.

Who should talk to the insurance company?

Ideally, not just the family. The strongest claims usually involve the treating physician, hospital case management, and the transport coordinator all providing consistent information. A family can push the process forward, but the medical record has to carry the argument.

If you're facing an active transfer and need help organizing the hospital, insurer, and transport steps, contact the team at Med Jets by Air Trek for current guidance on clinical coordination and coverage review.