When a hospital clinician says your family member needs to move today, the insurance question starts immediately. Can this ambulance or air ambulance be covered, and what has to happen before the claim is denied?

I have this conversation with families and case managers when the clock is already running. One physician is trying to secure an accepting bed. A bedside nurse is preparing records. Meanwhile, someone has to decide whether the patient can go by basic ground ambulance, critical care transport, or aircraft. The mistake I see most often is assuming the mode of transport decides coverage. Insurers usually start with a different question. Why was this level of transport medically required for this patient, on this date, to this destination?

The financial risk is real, especially if no one verifies the order, the destination, and the documentation before transport is booked. Even covered trips can leave a large balance when the claim is coded at the wrong level, the insurer disputes medical necessity, or the transport provider is outside the patient’s plan terms.

Start with a short checklist. Ask who the payer is today, not last month. Ask which clinician is ordering the transport. Ask why a lower level of service is not safe. Ask where the patient is going and why that destination is approved. Then ask for copies of the face sheet, the physician certification if one is being used, the transfer note, and the ambulance or flight medical necessity documentation.

One sentence can save hours later: “Please document why this patient cannot safely travel by a lower level of transport, and send me the ordering note and destination acceptance.” Families rarely hear that script, but it helps frame the claim the way insurers review it.

The Urgent Question Does Insurance Cover This Ambulance

A transfer decision often lands in the middle of a crisis. The ICU team says the patient needs a higher level of care. The receiving hospital is ready. Then the family hears two more words that can change the bill by thousands: ground ambulance or air ambulance.

I have seen families assume that if a doctor orders the transport, insurance will pay. That assumption causes problems. An order helps, but coverage usually turns on a tighter question: did the patient’s condition require this level of transport, to this destination, at this time?

That question gets harder in real cases. A bedside nurse may be calling report, a case manager may be trying to secure acceptance, and the family may be asked to sign transport paperwork before anyone has explained whether the claim will be treated as emergency, interfacility, in network, out of network, or partly noncovered. Air ambulance cases raise the stakes even more because the transport is expensive and the documentation standard is usually examined closely.

Why families get surprised by the answer

“Is it covered?” sounds simple. It is not a yes-or-no question.

Coverage can mean the plan has an ambulance benefit. It can mean the insurer accepts the trip as medically necessary. It can mean the destination meets plan rules. It can also mean the claim is covered but the patient still owes deductible, coinsurance, or charges the plan does not fully pay.

That is why I tell families and discharge planners to ask a better question: “What has to be documented for this exact transport to be covered, and who is confirming that now?”

What to confirm before anyone books the trip

Use this short check before the wheels move:

- Who is the active payer today? Coverage problems start with outdated insurance information.

- Who is ordering the transport? Get the ordering clinician’s name and note.

- Why is a lower level of transport unsafe? This is often the key sentence in the whole claim.

- Why this destination? The chart should show why the patient is going there and that the facility can provide the needed care.

- What level of ambulance is being requested? Basic ground, advanced life support, critical care transport, fixed-wing, and helicopter are reviewed differently.

- Is the provider in network, and if not, who approved using them? Families often miss this until the bill arrives.

- What paperwork can you get before departure? Ask for the face sheet, transfer note, physician order, and any medical necessity form or flight request.

One practical script helps: “Please send me the physician order, the accepting facility information, and the note explaining why this patient cannot safely travel by a lower level of transport.”

Use that language early. It gives the insurer the same facts they will ask for later, and it gives the family or case manager a paper trail if the claim is challenged.

The expensive mistake is treating ambulance coverage like a transportation benefit. Insurers usually review it as a clinical services claim first, then a benefits claim second.

Understanding The Universal Rule Medical Necessity

Every payer has different forms, departments, and wording. The gate that matters most is the same: medical necessity.

Insurance doesn't pay for an ambulance because the ride was helpful, faster, or more comfortable. It pays when the patient’s condition required ambulance-level transport and the chart supports that conclusion. If the record suggests the patient could have gone safely by car, wheelchair van, or standard discharge transport, the claim gets much harder to defend.

What medical necessity usually means in practice

For emergency calls, medical necessity is often tied to the clinical picture in real time. Dispatch notes, paramedic findings, oxygen needs, cardiac monitoring, stroke symptoms, trauma concerns, or the need for treatment during transport all matter.

For non-emergency transport, the standard is often stricter. The insurer may ask whether the patient was bed-confined, needed medical monitoring en route, required specialized handling, or couldn't tolerate ordinary transport because of the condition itself.

A simple working test helps:

| Question | Why it matters |

|---|---|

| Could this person travel safely another way? | If yes, ambulance coverage gets weaker |

| Did the patient need medical care during transport? | Supports ambulance-level necessity |

| Was the receiving facility able to provide needed care? | Helps justify destination |

| Does the chart clearly say why ground or air was required? | Weak documentation leads to denials |

Why insurers scrutinize these claims

Ambulance transport is expensive, and the price trend helps explain why payers review these claims so closely. Between 2017 and 2020, emergency ground ambulance charges for advanced-life-support services rose 22.6% from $1,042 to $1,277, while helicopter ambulance services increased 84% from $16,385 in 2012 to $30,151 in 2021, according to this FAIR Health ambulance cost study.

That doesn't mean every denial is justified. It does mean every claim reviewer is looking for a tight match between the patient’s condition and the transport used.

What works and what usually fails

What works is specific clinical language. “Patient required continuous cardiac monitoring,” “unable to tolerate ground duration due to condition,” or “receiving facility accepted for service unavailable at sending hospital” is useful when true and documented.

What fails is vague wording. “Family preferred transfer,” “doctor wanted a larger hospital,” or “faster and easier” usually doesn't carry a claim by itself.

If the chart doesn't explain why another transport mode was unsafe, the insurer may decide the ambulance was optional even when the family felt it clearly wasn't.

For families, this is the key point to remember: the medical team treats the patient first, but the insurer pays based on what the record proves.

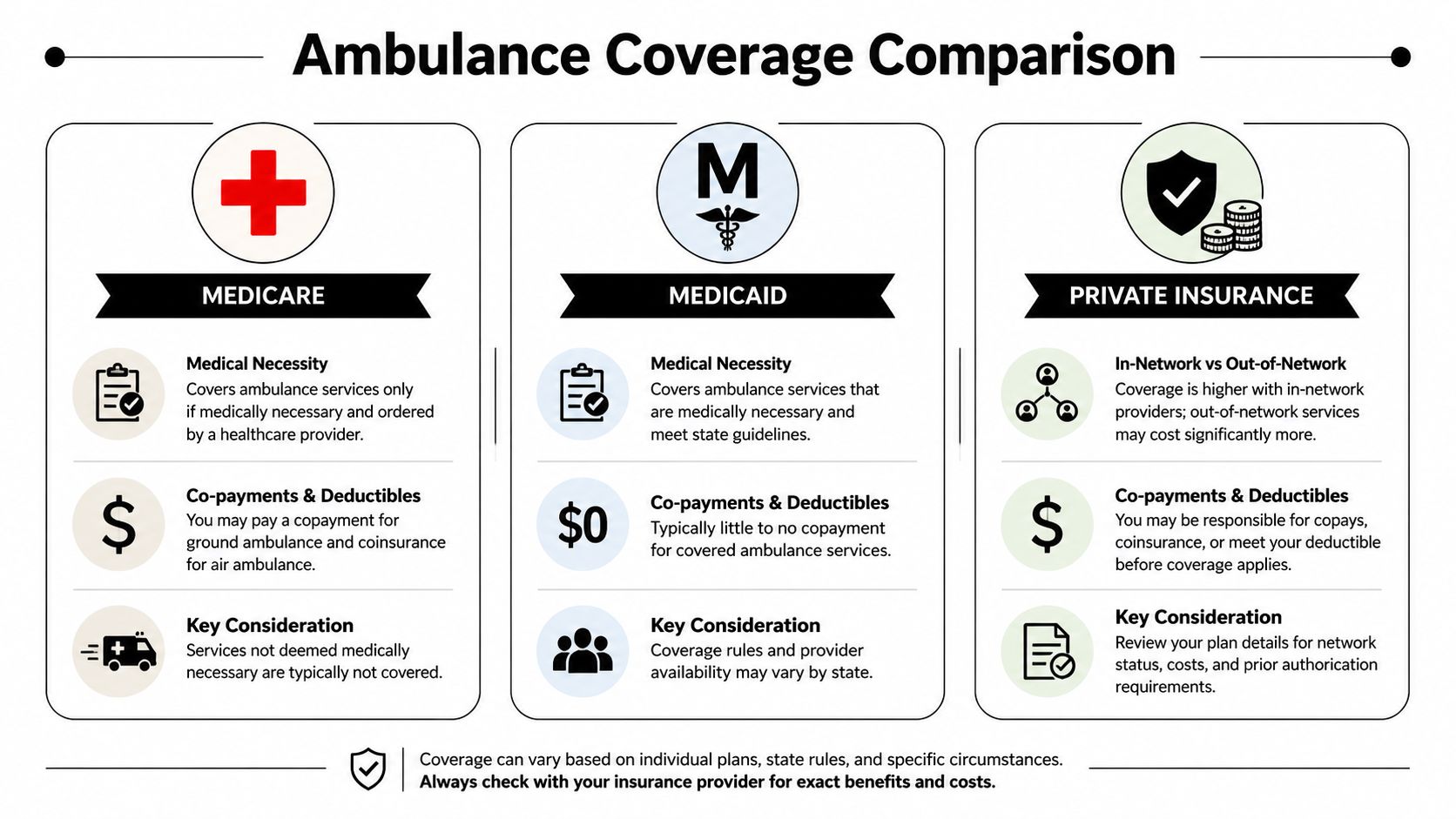

How Medicare Medicaid and Private Insurance Cover Ambulances

The answer to “does medical insurance cover ambulance” changes with the payer. The same patient, same diagnosis, and same destination can be reviewed differently depending on whether the coverage is Medicare, Medicaid, or a private plan.

Medicare

Medicare Part B is strict about destination. Coverage is generally limited to transport to the nearest appropriate medical facility capable of providing the needed diagnostic or therapeutic service, based on the Medicare ambulance policy manual.

That nearest-facility rule matters in both ground and air cases. If a patient is taken farther because the family prefers another hospital, the physician likes a different system, or a specialty center is chosen without clear medical justification, coverage can break down.

For air transport, documentation is especially important. A Physician Certification Statement or similar pre-flight clinical documentation explaining why ground transport is contraindicated can make a real difference in how the claim is evaluated. Families who need a closer look at that rule can review this guide on whether Medicare covers air ambulance.

Medicaid

Medicaid usually covers medically necessary transport, but the practical rules vary by state and plan structure. That's the part families often miss.

Some Medicaid programs are fairly straightforward for emergency transports and more demanding for scheduled trips. Others rely heavily on prior approval, specific physician wording, or contracted transportation vendors. For case managers, this means you can't rely on a general “Medicaid covers ambulance” assumption. You need the state-specific answer and, if managed care is involved, the plan-specific one too.

Private insurance

Private plans are the most varied. The biggest issues are often:

- Network status: The transport provider may not be in-network even when the hospital is.

- Plan language: Some policies separate emergency transport from non-emergency or interfacility transport.

- Authorization: Scheduled transports often need approval in advance.

- Medical review: The insurer may approve one level of transport and deny another.

A family can do everything right clinically and still run into a billing problem if nobody checked whether the plan treats that ambulance provider as out-of-network.

Side by side practical differences

| Payer | Main coverage trigger | Common problem |

|---|---|---|

| Medicare | Medical necessity and nearest appropriate facility | Preferred or distant destination |

| Medicaid | Medical necessity plus state or plan rules | State variation and vendor requirements |

| Private insurance | Medical necessity plus policy terms | Network status and prior authorization |

Coordinator’s note: When the payer is unclear, verify whether the patient has original Medicare, a Medicare Advantage plan, Medicaid managed care, or a commercial plan. Those are not interchangeable from a transport billing standpoint.

Emergency Vs Non-Emergency Transport What Changes

An emergency ambulance and a scheduled medical transport may both involve the same patient and the same diagnosis. The workflow is completely different.

In a true emergency

In a 911 event or urgent hospital deterioration, transport usually happens first and coverage gets sorted out afterward. The field team or sending facility makes a time-sensitive clinical decision. Families usually don't get to compare provider contracts or ask for detailed preauthorization terms.

That doesn't mean documentation doesn't matter. It matters a great deal. It just gets created during and after the event through dispatch notes, run sheets, physician records, receiving hospital acceptance, and medical necessity review.

If you need a practical picture of what urgent arrangements can involve, this overview of emergency medical transport services is useful because it reflects the operational side families are often dropped into without warning.

In non-emergency transport

Scheduled transfers are where many avoidable mistakes happen. A patient may be stable enough to move tomorrow, but not stable enough to travel by ordinary means. That's the zone where families assume insurance will naturally step in. Often, it won't unless the process is handled correctly.

Non-emergency transport usually raises these questions:

- Was there prior authorization?

- Did a physician sign an order stating transport was medically necessary?

- Was the destination approved?

- Was the chosen transport level justified?

The paperwork difference

Emergency claims are often defended by event records. Non-emergency claims are often won or lost before departure.

A useful way to consider this:

- Emergency transport: Clinical urgency drives the move, paperwork follows.

- Non-emergency transport: Paperwork drives whether the move gets paid.

Families often hear, “We'll bill insurance.” For non-emergency transport, that statement doesn't mean the insurer has approved anything.

If the move is scheduled, don't treat “medically necessary” as a verbal concept. Treat it as a document package.

Your Step-By-Step Guide to Arranging Medical Transport

When the transport isn't an immediate 911 event, a structured process saves money and time. In this scenario, families and case managers can still influence the outcome.

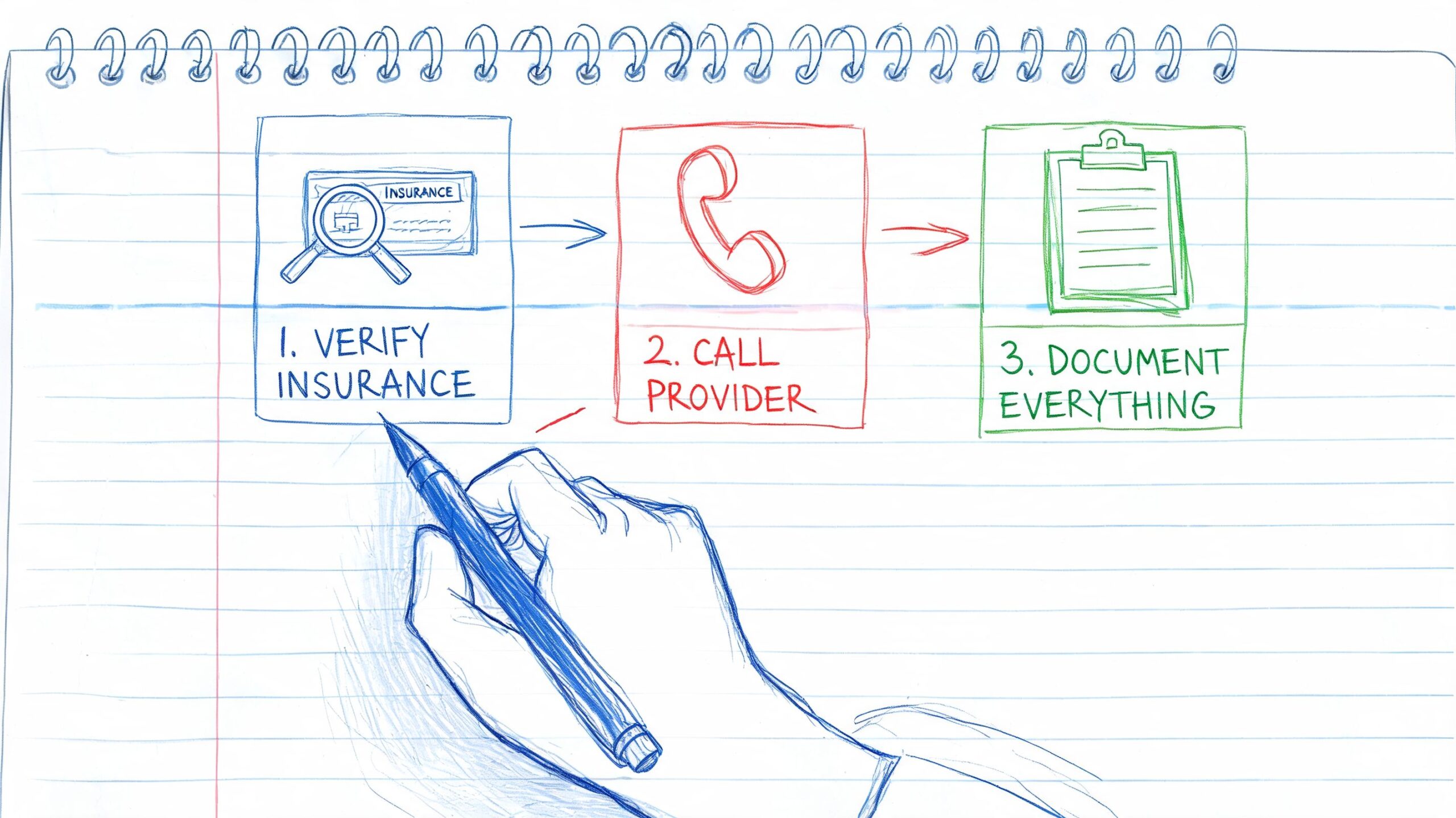

Step 1 Verify the exact benefit

Call the insurer before the trip, if the situation allows. Don't ask broad questions. Ask transport-specific ones.

Use wording like this:

- Coverage question: “Does this plan cover medically necessary ground ambulance or air ambulance transport for this member?”

- Authorization question: “Does this transport require prior authorization or pre-certification?”

- Level-of-care question: “What documentation is needed to approve this level of transport?”

- Destination question: “Does the receiving facility need to be the nearest appropriate facility under this plan?”

- Billing question: “How will out-of-network ambulance claims be handled under this benefit?”

Write down the date, time, representative name, reference number, and exact wording used.

Step 2 Get the physician documentation early

Many cases often stall because insurance policies require prior authorization for non-emergency transport based on a doctor’s written order, but patients and case managers can hit a real prior authorization paradox when physicians are hesitant or don't have the administrative support to complete the paperwork, as described in this ambulance coverage explanation from Gold Cross.

What helps is being very specific with the ordering team. Don't ask for “something saying transport is needed.” Ask for documentation that states:

- Why ordinary transport is unsafe

- What monitoring or interventions are required during transit

- Why the receiving facility is appropriate

- Why ground is contraindicated, if air is being considered

- Whether the patient needs stretcher, oxygen, bariatric accommodation, isolation, or clinical escort

Step 3 Work with a transport coordinator

A good coordinator closes the gap between medicine, logistics, and insurance language. That can be a hospital transfer center, a contracted ambulance service, or an air medical coordinator. One option in this category is Med Jets by Air Trek, which coordinates air ambulance, medical escort, and ground logistics for bed-to-bed transfers.

A coordinator should be able to tell you what records are still missing, what the sending physician must sign, whether the receiving hospital has accepted the patient, and what timing constraints could affect approval.

Step 4 Keep a clean paper trail

Create one file, digital or physical. Put everything there.

Include:

- Insurance notes: benefit calls, reference numbers, emails.

- Clinical records: face sheet, physician order, transfer summary, nursing notes if relevant.

- Transport records: quote, mode of transport, scheduled time, service level.

- Acceptance records: receiving physician or facility acceptance details.

This video gives a helpful overview of transport coordination issues families commonly face before a flight is arranged.

Step 5 Ask one question people forget

Ask, “If this claim is denied, what was the most likely missing piece?”

That question often gets a more useful answer than “Is it covered?” It forces the payer or coordinator to identify the weak spot before departure, while there's still time to fix it.

Understanding and Fighting Surprise Ambulance Bills

A bill can arrive even when the transport was medically necessary. That's why post-transport review matters almost as much as pre-transport planning.

The first document to study isn't always the invoice. It's the Explanation of Benefits, or EOB. The EOB tells you how the insurer processed the claim, whether the service was denied, applied to deductible, reduced for network reasons, or limited because the plan questioned medical necessity. If you need a plain-language primer on processing medical claims, that resource is useful for families reading an EOB for the first time.

What surprise billing looks like in ambulance cases

The most common issues are:

- Out-of-network processing

- Partial payment for a lower level of service

- Denial based on destination

- Denial based on lack of medical necessity

- Balance billing after insurance pays only part of the claim

One major source of confusion is the No Surprises Act. Since January 2022, it has offered protection against surprise billing for air ambulance services but not ground ambulance transportation, creating a gap many patients don't understand, according to this consumer explanation of ambulance surprise billing rules.

That means families may hear “surprise billing protections” and assume all ambulance bills are covered the same way. They aren't.

What to do when the bill looks wrong

Start with a focused review:

| Document | What to check |

|---|---|

| EOB | Denial reason, patient responsibility, network status |

| Ambulance bill | Dates, origin, destination, service description |

| Medical record | Whether it supports the transport level billed |

| Authorization record | Approval number or proof that no authorization was required |

Then act in order.

- Call the insurer first: Ask for the denial reason in plain language.

- Call the transport provider next: Ask whether they have additional records to submit or a billing review team.

- File an appeal promptly: Use physician documentation and transport records.

- Request itemized support: Especially if the level of service or destination rationale is disputed.

If you're trying to understand the broader financial side of flight arrangements before or after a claim issue, this guide to medical flight transport cost helps frame the kinds of charges families may encounter.

A denied claim isn't always the final answer. Many ambulance disputes come down to documentation that was incomplete, delayed, or reviewed without enough clinical context.

Ambulance Insurance FAQs and Communication Scripts

Families usually ask the same practical questions. The answers depend on plan language, but the questions themselves are worth using.

Quick answers families often need

Can I choose any hospital?

Not safely as an insurance assumption. Coverage may depend on whether the destination was the nearest appropriate facility or otherwise justified by the patient’s condition and plan rules.

If a doctor says the transfer is needed, is it covered?

Not automatically. A physician’s opinion is important, but the insurer still reviews medical necessity, destination, authorization, and policy terms.

What if the first claim is denied?

Ask for the exact denial reason, request the claim notes if available, and compare the denial to the physician order and transport chart. Many denials become clearer once you identify whether the issue was medical necessity, destination, coding, or missing authorization.

Script for calling the insurer

Use this script and take notes as you go.

“I'm calling to verify benefits for medically necessary ambulance transport for [patient name]. I need to confirm whether the plan covers ground ambulance, air ambulance, or both. Is prior authorization required for this type of transport? What clinical documentation is needed? Does the plan require transport to the nearest appropriate facility? Is the provider required to be in-network? If the transport is out-of-network, how is the claim processed? Please give me the reference number for this call.”

Then ask one follow-up question:

“If this claim were denied, what would be the most common reason?”

That answer often tells you exactly what document to chase.

What to say to the physician office or hospital team

Keep it simple and specific:

- “Please document why ordinary transport is unsafe.”

- “Please document what care is required during transit.”

- “Please document why this receiving facility is medically appropriate.”

- “If air transport is being requested, please document why ground transport isn't appropriate.”

When families use precise language, the paperwork gets better. Better paperwork gives the claim a better chance.

If you're arranging a complex transfer and need help sorting out the clinical and logistics side before transport is booked, contact a qualified ambulance or air medical coordinator early. The safest transport and the most defensible insurance file are usually built at the same time.