The call usually comes at the worst possible moment. Your phone lights up. A nurse, physician, or case manager tells you your spouse, parent, or patient is stable enough to move, but not safe to travel on a commercial flight. They need an air medical transport. Then the next question lands fast: who's paying for this?

Most families freeze right there. Not because they don't care, but because air med insurance is one of the least understood parts of emergency planning. People mix up health insurance, air ambulance billing, membership programs, transfer coordination, and the No Surprises Act. Under stress, those details blur together.

That confusion gets expensive.

I've seen the same pattern again and again. A family assumes their health plan “covers air ambulance.” A discharge planner assumes the transport company will sort out bedside-to-bedside logistics. Someone else assumes federal law means there's no real bill risk anymore. None of those assumptions are safe.

If you're making this decision now, you need three things. A clear view of what kind of transport is being requested. A hard look at what your policy pays for. And a coordinator who can move records, physicians, ground legs, and receiving-facility acceptance without dropping the ball. Companies such as Med Jets by Air Trek handle that kind of end-to-end medical transport coordination, but the bigger point is this: you need answers before the aircraft is booked, not after the claim is denied.

The Urgent Call You Never Expect to Receive

A daughter gets a call that her father collapsed while traveling. He's been treated at a regional hospital. He's no longer in immediate danger, but the treating team wants him moved to a larger facility closer to home for continued care.

She hears phrases like “medical necessity,” “accepting physician,” and “air ambulance authorization,” but what she really hears is panic. Is the transfer covered? Can he go to the hospital the family prefers? Can someone fly with him? Does the hospital arrange this, or does she?

That moment is where bad assumptions start. Families often think an air transfer is just a flight with a stretcher. It isn't. It's a clinical handoff, a transport decision, a billing event, and a logistics operation all at once.

What matters in the first hour

The right first question isn't “How much does it cost?”

It's “Why is the patient being moved, and who documented that reason?”

If the transfer is medically necessary, every detail that follows gets easier. If the reason is loosely described as convenience, family preference, or a general desire to be closer to home, the billing risk climbs fast.

The safest path is simple: get the clinical reason for transfer stated clearly by the treating physician before anyone argues about benefits.

What families and case managers should do immediately

- Ask for the transfer rationale: Get the sending physician's medical reason in plain language.

- Confirm the receiving facility: A bed, an accepting physician, and the service line must be lined up.

- Identify the decision maker: One family contact or one case manager should handle updates.

- Pause before signing broad financial forms: Read transport paperwork closely. Ask what is being authorized.

When people are scared, they rush to “just get them home.” I understand that instinct. But air med insurance disputes usually start with rushed paperwork and weak documentation, not with the flight itself.

Decoding Air Med Insurance and Memberships

People use air med insurance to mean two very different things. That's the first problem.

One model is a membership program. It's comparable to AAA for medical flights. You pay in advance, usually annually, and the program may arrange or cover certain transport costs under its rules.

The other model is traditional health insurance reimbursement. That means the flight is billed as a medical claim, and the insurer decides what it will pay based on medical necessity, plan terms, network status, and exclusions.

The practical difference

Memberships are about access and financial protection under a program's conditions. Health insurance is about claim adjudication after the transport is justified and billed.

That's why people get tripped up. They think a membership replaces health insurance, or they think health insurance guarantees a full payment. Neither is a safe assumption.

If you're comparing options, start with a plain-language overview of medical flight insurance options, then match that against the patient's actual medical and travel profile.

Air Med Membership vs. Insurance Reimbursement

| Feature | Air Med Membership | Traditional Health Insurance |

|---|---|---|

| How you pay | Annual fee paid in advance | Premiums paid as part of your health plan |

| Primary purpose | Transport protection or coordination under membership terms | Reimbursement for covered medically necessary care |

| When it helps most | Planned risk protection before a crisis | After a covered claim is submitted |

| Decision trigger | Membership rules and service area terms | Medical necessity and policy language |

| Transfer type focus | Often useful for arranged transport scenarios | Strongest when the transport qualifies as a covered medical claim |

| Family expectation | “We joined a program” | “We have health insurance” |

| Common mistake | Assuming every requested flight qualifies | Assuming every air transport is paid in full |

What to ask before you rely on either

- Membership scope: Does it apply only to certain transports, regions, or aircraft arrangements?

- Insurance definition: What exactly does your health plan call medically necessary air transport?

- Ground transport handling: Are bedside-to-bedside legs included, coordinated separately, or excluded?

- Approval path: Is pre-authorization required when the transfer isn't a scene emergency?

If you can't explain in one sentence why the patient needs this aircraft, this crew, and this destination, you're not ready to assume the bill will be covered.

My recommendation is blunt. Don't buy or rely on any air med product you can't explain to a stressed family member in under two minutes. If the terms are muddy, the claim risk is real.

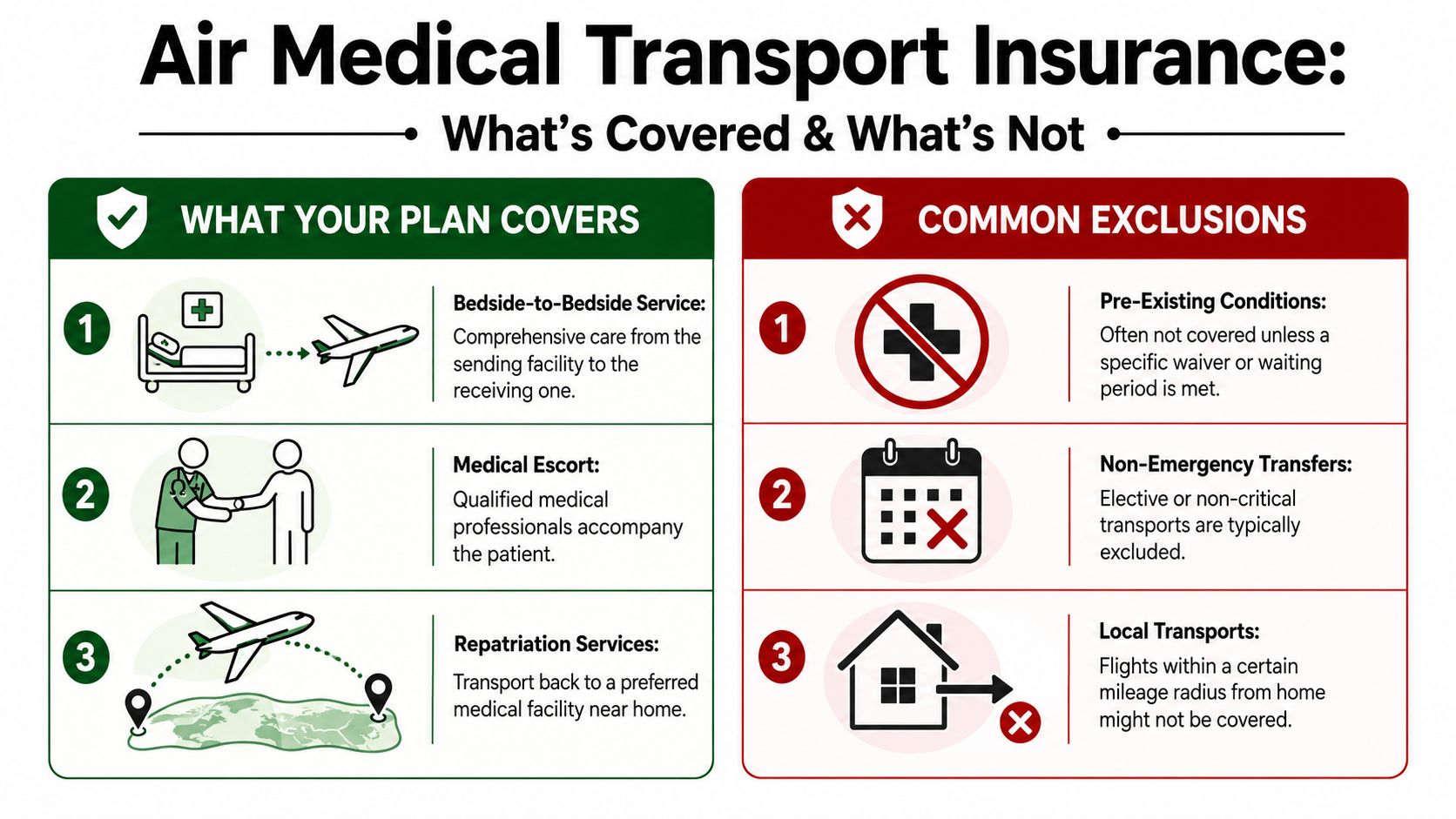

What Your Plan Actually Covers and Excludes

Coverage decisions usually turn on one phrase: medical necessity. Not family preference. Not convenience. Not “the hospital suggested it.” Medical necessity.

The South Carolina Department of Insurance notes that reimbursement can hinge on the policy's definition of medical necessity and the transport configuration, including whether services such as oxygen or life support are provided during transport, whether a specific aircraft type is required, and whether bedside-to-bedside ground legs or family accompaniment are included in the billed service, as outlined in its consumer alert on air ambulance insurance.

Medical necessity means the transport has to be clinically justified under the plan's rules, with the right level of care, the right mode of transport, and the right destination documented clearly.

What's commonly included

- Clinical care in transit: If the patient needs active monitoring or treatment during the flight, that clinical component matters.

- Specific onboard support: Oxygen, life support measures, and a qualified medical team can be part of the covered transport setup.

- Ground coordination: Some policies recognize bedside-to-bedside service, which means the trip starts at the sending facility and ends at the receiving one, not just airport to airport.

What often gets denied or limited

- Convenience transfers: Wanting a patient closer to home isn't the same as meeting the insurer's medical standard.

- Wrong aircraft choice: If the plan says a lower level of transport would have been adequate, reimbursement can be cut or denied.

- Incomplete transfer chain: If ground legs, accompanying family travel, or origin and destination details aren't documented properly, the insurer may split the claim or reject part of it.

The paperwork that decides the outcome

Families focus on the aircraft. Case managers know the file matters more.

Here's what should be locked down before departure whenever possible:

- Physician certification: The sending doctor should state why air transport is required.

- Origin and destination records: Names of facilities, care levels, and accepting provider details should match across all documents.

- Authorization trail: If pre-authorization applies, get it documented. If it can't be obtained in time, document why.

- Transport scope: Clarify whether the quote and the claim include ground legs, onboard care, and family accompaniment.

A weak file turns a real medical transfer into an argument. A strong file gives the insurer less room to reframe the flight as optional.

The True Cost of Air Medical Transport

Air medical transport is expensive because you're not buying a seat. You're buying an aircraft, a medical environment, a trained crew, dispatch coordination, and time-sensitive logistics.

The National Association of Insurance Commissioners says the average U.S. air ambulance trip is about 52 miles and costs between $12,000 and $25,000 per flight, and more than 550,000 patients in the U.S. use air ambulances each year, according to the NAIC's consumer guidance on air ambulance coverage.

Why the bill gets high fast

The aircraft is only one part of it. The transport team has to match the patient's condition. Dispatch has to coordinate hospitals, records, and timing. Ground transport may need to be arranged at one or both ends.

If you want a useful breakdown before you call, this guide on what impacts air ambulance pricing and what you'll be asked is a practical place to start.

This short video also helps frame what drives transport pricing in practical terms.

The premium comparison that gets attention

Annual membership-style premiums are often cited at about $85 to $100 for basic plans and roughly $200 to $500 for broader medevac-style memberships, as summarized in this overview of air ambulance insurance costs and market context.

That gap is why families even look at these products. The contrast between a yearly membership cost and a single flight bill is obvious.

My recommendation on cost planning

- If you travel often: Review transport protection before the trip, not during a hospitalization.

- If you manage discharges: Don't discuss price without also discussing scope. Ask what exactly the quote includes.

- If the patient is medically fragile: Get clear on transfer thresholds early. Waiting until a crisis narrows your options.

Cost alone shouldn't drive the decision. But ignoring cost is how families end up making rushed choices with the least advantage.

Does the No Surprises Act Make Coverage Obsolete

No. It changed the risk. It did not erase it.

This is the biggest source of bad online advice about air med insurance. People hear that the No Surprises Act protects patients from giant air ambulance bills and assume memberships or supplemental protection no longer matter. That's too simplistic.

The law bans surprise balance billing for covered emergency air transport for privately insured patients. It does not eliminate your plan's deductibles, copays, or coinsurance. It also doesn't turn every air transport into a paid claim.

What the law solved

Before these protections, patients were getting hit from two directions. They had the medical emergency itself, then they had a bill fight over out-of-network air ambulance charges.

One independent study found that fewer than one-quarter of commercially insured air ambulance transports were in-network, and 40% of helicopter rides could trigger a potential balance bill averaging $19,851 before the law's protections were considered, as reported in this peer-reviewed study on air ambulance balance billing.

That explains why the No Surprises Act matters. It addressed a real billing problem.

What the law did not solve

It did not eliminate ordinary patient cost-sharing.

It did not make non-emergency transfers automatically payable.

It did not remove the insurer's ability to scrutinize whether the flight met the plan's definition of medical necessity.

A federal billing protection is not the same thing as a blanket promise that the transport will be covered the way you expect.

So do you still need air med insurance

Sometimes, yes.

You should still take air med insurance or a membership seriously if any of these apply:

- High deductible health plan: You may still owe meaningful out-of-pocket costs even when protections apply.

- Frequent travel or seasonal relocation: Transfers home or to a preferred facility can fall into messy territory.

- Medically complex patient: The more specialized the transfer, the more important the documentation and coverage details become.

- Non-emergency transport concerns: Federal surprise-billing protections don't answer every transfer scenario families face.

The right way to think about it now

Don't ask, “Does the law mean I'm safe?”

Ask, “What costs remain if the transport is covered, and what happens if the insurer disputes the claim at all?”

That's the modern question. If you're a case manager, make that part of every family conversation. If you're a family member, don't let anyone wave away the financial side with a vague mention of federal law.

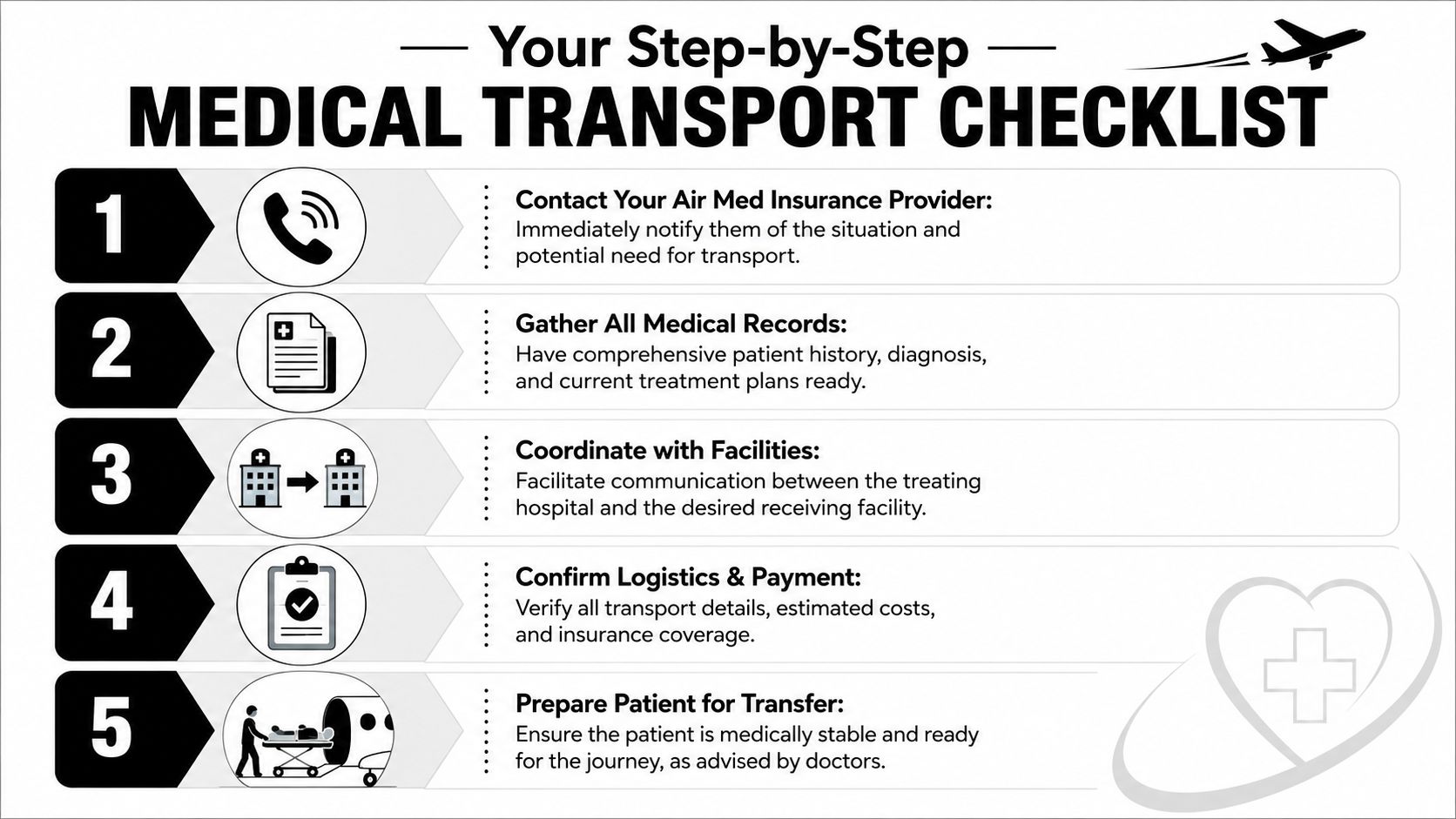

Your Step-by-Step Medical Transport Checklist

When a transfer is moving quickly, people miss steps that later become billing problems. Use a checklist. It keeps everyone aligned and cuts down on avoidable mistakes.

Step 1 Call the transport coordinator

Call the air ambulance provider or coordinating service as soon as the treating team says transfer is likely. Don't wait for every record to be perfect before making first contact.

Have these ready:

- Patient identity details: Full name, date of birth, current location

- Clinical summary: Diagnosis, current condition, isolation status if relevant

- Hospital contacts: Sending nurse station, case manager, treating physician

Step 2 Gather the medical file

The transport company and insurer both need the same core story. Why does this patient need this transfer now?

Collect:

- Recent physician notes

- Medication list

- Vital transport requirements: Oxygen, monitoring, mobility, special handling

- Receiving acceptance details: Facility name and accepting physician

Practical rule: If the sending and receiving hospitals are telling different versions of the patient story, stop and reconcile that before wheels up.

Step 3 Verify insurance or membership terms

Families often get vague reassurance instead of specifics. Don't accept that.

Ask for:

- Whether pre-authorization is required

- How the plan defines medical necessity for air transport

- Whether bedside-to-bedside ground legs are included

- What patient cost-sharing still applies

- Whether a family member can accompany the patient under the transport arrangement

Step 4 Confirm logistics from bed to bed

An air transfer fails in the margins, not in the air. Someone needs to own the handoff points.

Use this quick operational checklist:

| Item | What to confirm |

|---|---|

| Sending facility | Patient is medically ready and records are released |

| Receiving facility | Bed is available and physician has accepted |

| Ground transport | Pickup and drop-off legs are arranged if needed |

| Family communication | One point person gets all updates |

| Financial paperwork | Authorization and responsibility forms are reviewed |

Step 5 Prepare the patient and family

The patient may need medication timing adjusted, equipment prepared, or personal items limited. Families should know what they can bring, whether they can ride along, and where they'll meet the patient after arrival.

Good transport teams explain this clearly. If the instructions are confusing, ask again until they aren't.

Key Questions for Your Provider and Insurer

If you ask weak questions, you get vague answers. Ask direct questions and wait for direct responses.

A short read on understanding prior authorization for medical transport can help you frame these conversations before you call.

Questions for your insurance company

- How does my plan define medical necessity for air transport?

- Is this transfer treated as emergency transport or a scheduled interfacility transfer?

- Do I need pre-authorization, physician certification, or both?

- What part of the transport is subject to deductible, copay, or coinsurance?

- Are ground ambulance legs included when the transfer is arranged bedside to bedside?

- Does the destination have to be the closest appropriate facility, or can the patient go to a preferred hospital?

- If the claim is denied, what is the appeal path and what documents will matter most?

Questions for the air ambulance provider

- Are you the direct operator or are you brokering the trip?

- What level of medical crew will be on board for this patient's condition?

- What exactly is included in the quote or transport agreement?

- Are bedside-to-bedside ground segments part of the arrangement?

- Can a family member travel with the patient, and under what conditions?

- What records do you need from the sending hospital before launch?

- Who is responsible for coordination with the receiving hospital?

- How will billing be submitted, and who will communicate with the insurer?

The questions that protect you most

Three questions matter more than the rest:

- Why is this transport medically necessary?

- What exactly is included in the service?

- What can still become my responsibility financially?

If you don't get clean answers, slow the process down long enough to get them. Fast action matters in medical transport. So does disciplined coordination.

If you're evaluating air med insurance, don't settle for broad promises. Match the policy or membership to the actual transfer risk, the patient's condition, and the billing gaps that still exist after federal protections. That's how families avoid confusion, and how case managers avoid preventable disputes.