The call usually comes without warning. A spouse is on a business trip, a parent is on a cruise extension, or a college student is visiting friends across the country. Then someone says the words families dread: “They're in the hospital, and the doctors may need to transfer them.”

At that point, people don't ask technical insurance questions first. They ask practical ones. Can we get them closer to home? Who decides? How fast can this happen? And who's going to pay for it?

Those questions get harder when the patient is stable enough to move, but not simple enough to put on a regular flight. That's where medical flight insurance enters the picture. It isn't just about an airplane. It's about whether a transfer qualifies, whether the paperwork supports it, and whether the insurer agrees the move is medically necessary.

I've seen families focus on the policy name while the actual issue sits in the chart notes. In many cases, the documentation of medical necessity matters more than the headline promise of “evacuation coverage.” If the record doesn't clearly show why the patient must fly, where they must go, and why another option won't work, coverage can fall apart even when a policy exists.

A Medical Crisis Far From Home

A daughter gets a call that her father collapsed while traveling. He's awake now, but confused. The local hospital can stabilize him, not manage the specialty care he needs. The family wants him transferred to a larger center, preferably near home, where his own doctors can step in and decisions won't happen over speakerphone.

That's the moment people discover how many moving parts sit behind a medical flight. A sending physician has to document the patient's condition. A receiving hospital has to accept the transfer. Someone has to decide whether the patient needs a dedicated air ambulance, a commercial flight with a medical escort, or ground transport. Insurance has to be notified. Records have to move fast.

What feels like a rare disaster is more common than most travelers realize. The broader market reflects that. The global travel insurance market was valued at USD 27.05 billion in 2024 and is projected to reach USD 63.87 billion by 2030, according to Grand View Research's travel insurance market report. Medical transport is part of that larger protection category, which tells you this isn't a fringe concern.

What families feel in the first hours

The first problem is emotional. People hear “transfer” and assume the obvious answer is to book a flight. It rarely is.

The second problem is administrative. Hospitals, insurers, and transport coordinators all use different language for the same situation. A family says, “Bring him home.” The insurer asks, “Is transfer to the nearest adequate facility medically necessary?” Those are not the same question.

The family's goal is usually comfort and familiarity. The insurer's test is usually necessity and appropriateness.

What helps right away

In the first conversation, these are the details that matter most:

- Current hospital status: Is the patient in ICU, telemetry, emergency observation, or a regular room?

- Clinical reason for transfer: What treatment, specialist, or level of care is unavailable where the patient is now?

- Receiving facility: Has another hospital formally agreed to accept the patient?

- Transport tolerance: Can the patient sit upright, travel on oxygen, or require full monitoring and stretcher care?

When those facts are clear early, decisions move faster. When they're vague, everyone loses time.

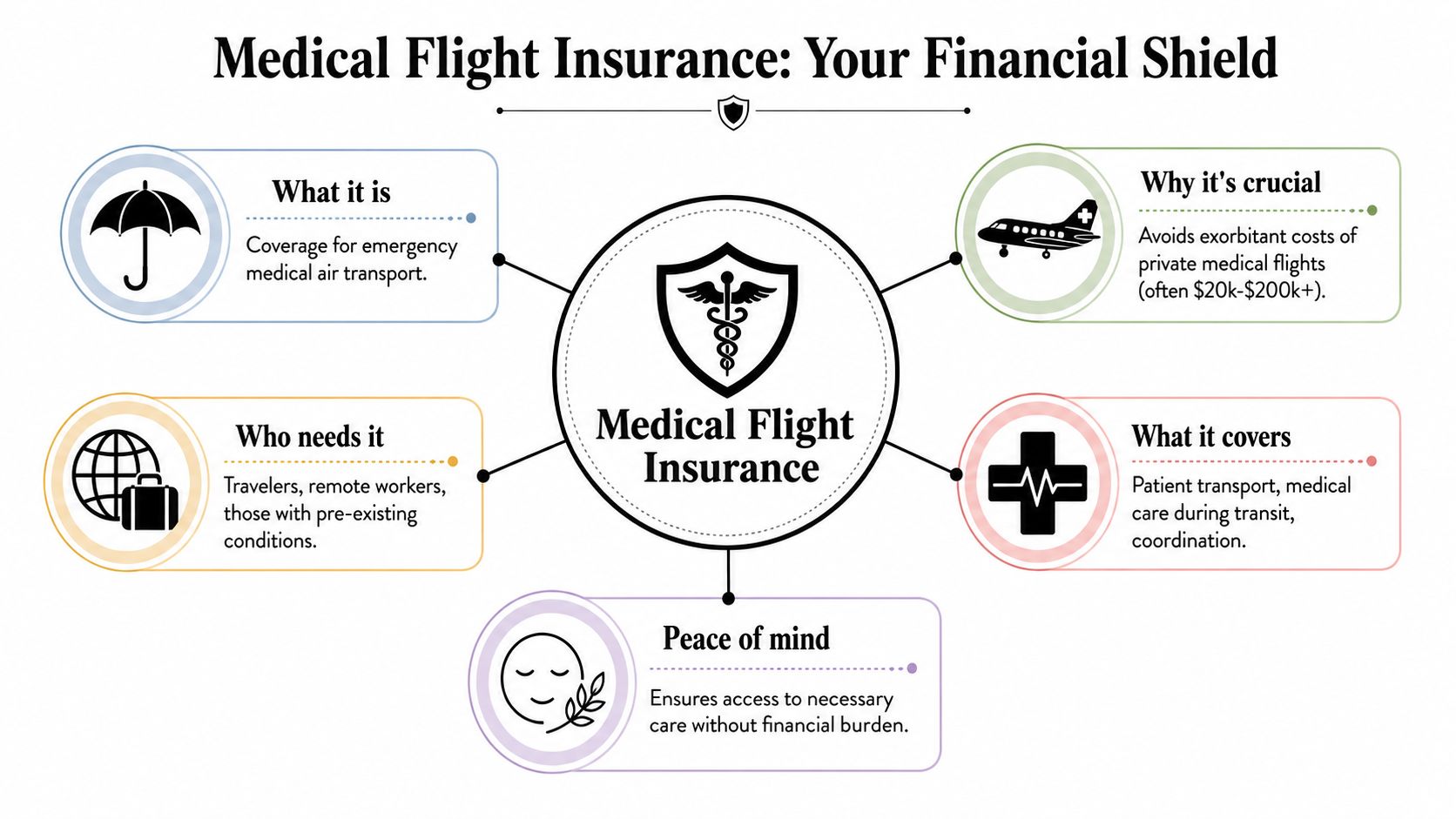

Understanding Medical Flight Insurance

Medical flight insurance is best understood as financial protection for medically necessary transport when a patient can't safely travel by ordinary means. Sometimes that means a dedicated air ambulance. Sometimes it means a commercial aircraft with a nurse or paramedic escort. The right option depends on the patient's condition, not the family's preference.

What the flight actually pays for

A lot of people imagine the aircraft is the whole service. It isn't. The aircraft is only one piece of the transfer.

A true medical flight can function like a flying ICU or a flying monitored room, depending on the patient's needs. Coverage may involve:

- Aircraft and crew: The plane, pilot team, and medical personnel.

- In-transit care: Oxygen, monitoring, medication management, and life-support capability when required.

- Ground links: Ambulances from hospital to airport and airport to hospital.

- Coordination work: Physician communication, records transfer, scheduling, and clearance logistics.

The price is why this matters. The NAIC says the average 52-mile air ambulance trip in the U.S. costs between USD 12,000 and USD 25,000, and for longer or more complex international situations, costs can exceed USD 200,000, as outlined in the NAIC consumer guide to air ambulance coverage.

Later in the process, families often need a plain-language overview. This short video helps explain how air ambulance services fit into the broader medical transport decision.

Medical evacuation versus repatriation

These terms get mixed up constantly.

Medical evacuation usually means moving the patient to the nearest adequate facility that can provide the required treatment. That's a clinical decision.

Medical repatriation usually means returning the patient to their home country, home region, or preferred hospital after stabilization. That's a different benefit, and some policies handle it much more narrowly.

Practical rule: If the patient needs a higher level of care right now, think evacuation. If the patient is stable and the goal is getting home for ongoing care, think repatriation or escorted transport.

Who tends to need it

Medical flight insurance matters most for people who are:

- Traveling internationally: Ordinary health coverage often becomes harder to use across borders.

- Far from tertiary care: Rural, island, cruise, or remote settings create transfer problems fast.

- Managing fragile health: Cardiac, neurologic, respiratory, bariatric, and post-surgical patients often need specialized planning.

- Traveling with assumptions: Many people believe their health plan or credit card protection will handle transport. Sometimes it won't.

The core value isn't just payment. It's whether the patient can reach appropriate care without placing the entire financial and logistical burden on the family.

Who Actually Pays for a Medical Flight

Most families assume there's one clear payer. In practice, payment responsibility often sits across several buckets, and each one uses different approval standards. The hardest part is that a “yes” to hospital care doesn't automatically mean a “yes” to medical transport.

Private health insurance

Private health insurance may cover an air ambulance, but only under strict conditions. In real-world cases, the plan usually asks whether the transport was medically necessary, whether the service level matched the patient's condition, and whether the destination made clinical sense.

If a patient can be treated locally, or if a lower-acuity option would have worked, the claim can run into trouble. If the transport goes to a preferred hospital instead of the nearest appropriate facility, that can also become a problem.

Medicare and Medicaid

Public coverage is where families often have the highest expectations and the biggest misunderstandings. These programs can be highly restrictive around transport, especially if the request looks like convenience, family preference, or relocation rather than urgent medical necessity.

Case managers know this well. A patient may absolutely need continued treatment, but the program may still decline the flight if the documentation doesn't support the mode of transport, the destination, or the timing.

Travel insurance

Travel insurance is often the most promising source for an out-of-state or international event, but it has a critical trigger. The transport must typically be medically necessary to the nearest adequate facility, not merely the hospital the family wants.

One consumer resource notes average air ambulance costs of about USD 36,000 to USD 40,000, and that misunderstanding the coverage trigger can leave the family with the bill, as explained in Angel Flight West's guide to air ambulance services for medical travel.

That's why I tell families to stop asking only, “Do we have coverage?” and start asking, “What event triggers this benefit?”

The comparison that matters

| Coverage Source | Likely to Cover? | Key Limitations |

|---|---|---|

| Private health insurance | Sometimes | Medical necessity, network rules, destination limits, authorization requirements |

| Medicare or Medicaid | Rarely for non-routine transfer goals | Narrow criteria, limited support for non-emergency return or preference-based moves |

| Travel insurance | Often for covered emergencies | Usually tied to nearest adequate facility, benefit caps, documentation and assistance-company approval |

| Membership program | Depends on program terms | Not insurance, service conditions apply, hospitalization and distance rules may control eligibility |

| Family self-pay | Always available if arranged | High financial exposure, especially when urgency limits shopping and planning |

What works and what doesn't

What works is early coordination among the treating doctor, receiving doctor, insurer, and transport coordinator. What doesn't work is booking first and arguing later, unless the situation is so urgent that no other path exists.

If you're trying to sort out the overlap between policies, public plans, and transport vendors, this breakdown of whether insurance covers air ambulance is a useful starting point.

The real gatekeeper is the chart

Families often think policy language is the main issue. It's only half the issue.

The chart has to answer key questions clearly:

- Why can't the patient stay where they are?

- Why is flight required instead of ground or commercial travel?

- Why is the receiving facility clinically appropriate?

- Is the patient stable enough to fly with the proposed level of care?

If those answers aren't explicit, denials become much more likely. The coverage may exist on paper and still fail in practice.

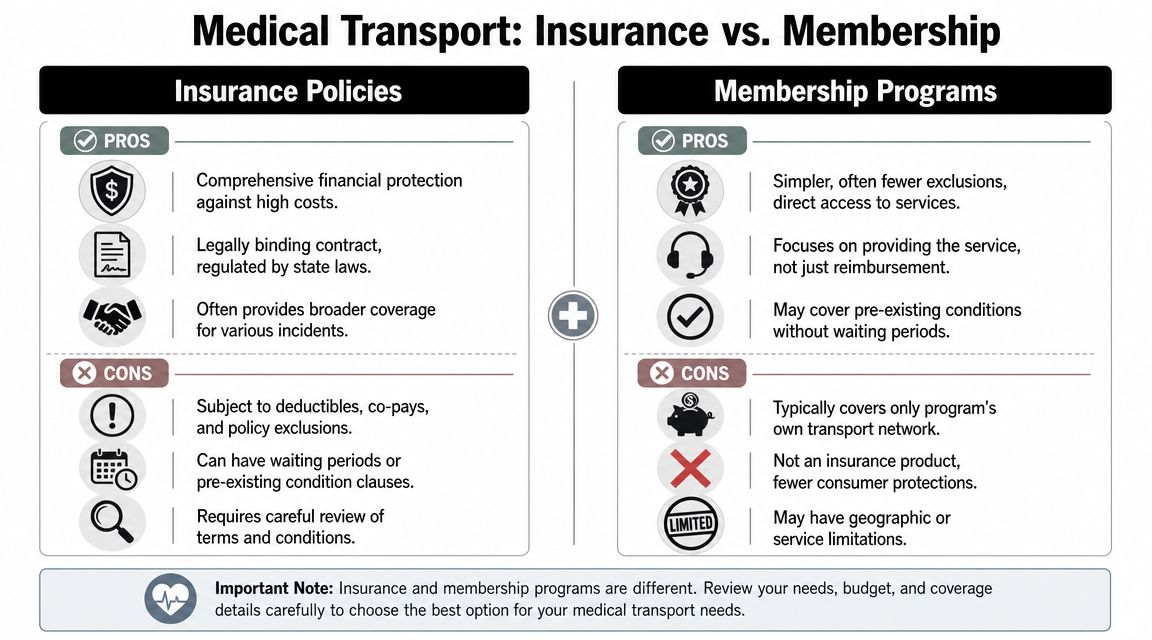

Membership Programs vs Insurance Policies

This is one of the biggest sources of confusion in medical transport. People search for medical flight insurance and end up comparing two products that are built on totally different models.

They solve different problems

An insurance policy usually pays or reimburses for a covered claim, subject to policy terms. A membership program usually promises to arrange and provide transport under specific conditions if a member qualifies.

That distinction matters. Angel MedFlight's explanation of transport memberships highlights that memberships are not technically insurance. That affects how consumers should think about exclusions, claims handling, and who pays the provider directly.

How the experience feels different

With insurance, the family often deals with approvals, benefit language, medical necessity review, and later claim administration. The stress point is uncertainty. You may have a covered event, but still need the right documentation and authorization path.

With a membership, the stress point is eligibility under program rules. The program may require hospitalization, distance from home, destination limits, or other conditions before it will activate transport.

A membership can feel simpler because it's service-focused. An insurance policy can feel broader because it's financially structured. Neither one replaces the need to read the terms.

A side-by-side practical view

| Model | What it primarily does | Best fit | Common friction point |

|---|---|---|---|

| Insurance policy | Pays or reimburses for covered medical transport expenses | Travelers who want financial protection within a broader travel policy | Claims language and approval criteria |

| Membership program | Arranges and provides transport under program conditions | People focused on return transport support when hospitalized away from home | Activation rules and service boundaries |

Which one makes more sense

A few decision questions usually bring clarity:

- Do you want reimbursement protection or arranged service? Those are different needs.

- Do you travel occasionally or constantly? Frequent travelers often care more about operational simplicity.

- Are you worried about emergency evacuation or getting home after hospitalization? Those are related but not identical use cases.

- Does the patient have pre-existing complexity? You need to read the definitions carefully, not rely on marketing shorthand.

For readers comparing these two paths in more detail, this overview of air evac insurance options helps frame the trade-offs in plain language.

Where families get tripped up

The most common mistake is assuming a membership equals unrestricted insurance coverage. It doesn't.

The second mistake is assuming insurance will arrange everything automatically. It may not. Some policies rely heavily on assistance companies, prior notice, and approved routing.

The right question isn't “Which is better?” It's “Which model matches the kind of transport problem I'm trying to solve?”

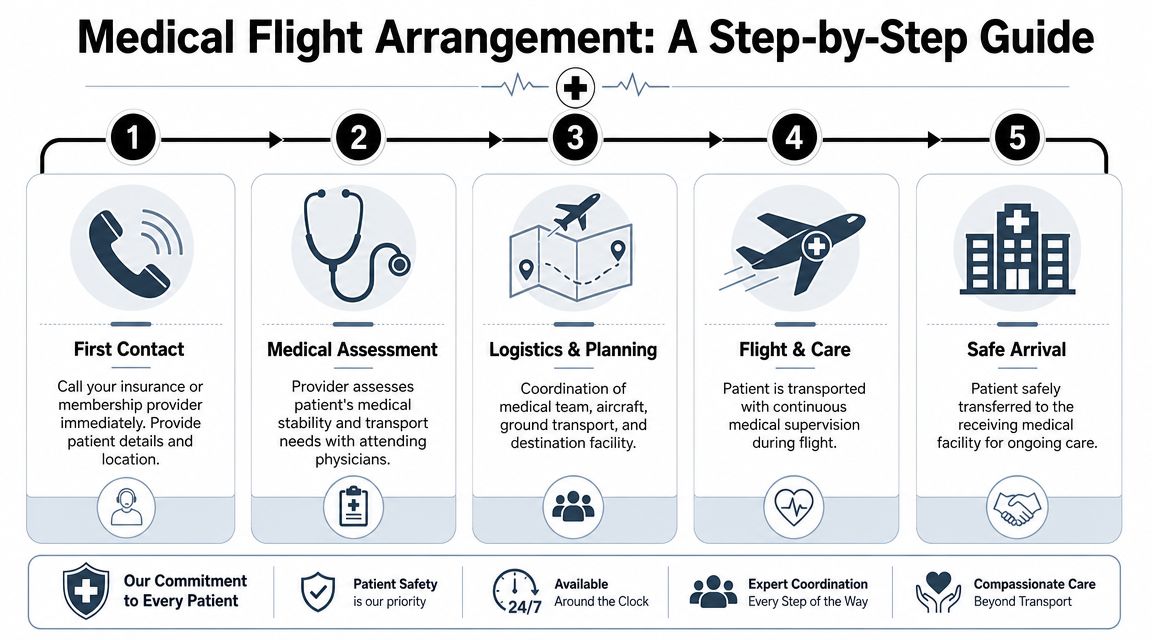

Arranging a Medical Flight Step by Step

When a transfer is needed, the fastest path is a disciplined one. Families lose time when they chase aircraft options before the medical case is built. The sequence matters.

Step 1 starts with medical necessity

Before anyone argues about payment, the sending team has to document why the patient needs to move. That note should explain the diagnosis, the current level of care, what treatment is unavailable locally, and why the proposed transport mode is appropriate.

If the patient could travel by less intensive means, someone needs to say why that won't work. If the destination is farther away than the nearest capable hospital, someone needs to justify that choice clinically.

Step 2 confirms the receiving plan

A transfer isn't real until the receiving facility accepts the patient. That means a doctor-to-doctor handoff, a bed assignment path, and a clinical reason for that receiving center.

The entire medevac chain matters. Squaremouth's explanation of medical evacuation and repatriation notes that coverage depends on medical necessity, coordination across transport segments, and the appropriateness of the receiving facility.

Step 3 gathers the documents that move the case

The essential elements usually include:

- Medical records: Recent physician notes, medication lists, imaging summaries, lab summaries, and nursing status.

- Insurance information: Policy numbers, contact numbers, and any travel assistance contacts.

- Identity documents: Passport or ID, especially for cross-border or international transfer.

- Consent and contact details: Family decision-maker, power of attorney if relevant, and bedside contact numbers.

If the paperwork lags, the aircraft waits. If the aircraft waits, the transfer window can close.

Step 4 builds the transport plan

Now the coordinator can match the patient to the right mode. Some patients need a dedicated jet with intensive monitoring. Others can safely move with a stretcher setup or a commercial medical escort.

One operational provider might enter the discussion. For example, Med Jets' fly-u-home medical transport services describe bedside-to-bedside coordination that can include air transport, escorts, and ground segments. That kind of end-to-end planning is often what families need, regardless of which provider they ultimately choose.

Step 5 manages handoff and arrival

The flight isn't the end of the process. Good coordination covers:

- Sending hospital release timing

- Ground ambulance to the departure airport

- In-flight clinical updates if needed

- Arrival ground transport

- Receiving facility handoff

What works is continuity. What fails is fragmentation, where one party assumes another party handled a detail that nobody confirmed.

Navigating Common Exclusions and Denials

Most denials are not mysterious. They usually trace back to a small group of recurring problems. Once you know them, you can prevent many of them.

The most common reasons claims fail

- Medical necessity wasn't documented clearly: The chart may say the patient wanted transfer, but not why flight was required.

- The destination looked elective: A return to a home hospital may feel reasonable, but the payer may treat it as preference rather than necessity.

- Authorization steps were missed: Some plans expect notice to the insurer or assistance company before transport, when circumstances allow.

- The transport level didn't match the patient's condition: If a lower-acuity option appears possible in hindsight, the more expensive flight may be challenged.

- Policy exclusions applied: Pre-existing condition language, high-risk activities, or travel-specific exclusions can affect eligibility.

How to reduce the risk before the flight

A clean file beats a passionate argument every time. Ask the clinical team to document in plain terms:

- Why the patient can't remain at the current facility

- Why the chosen receiving facility is appropriate

- Why air transport is necessary

- Why alternative transport is unsafe, unavailable, or inadequate

That language doesn't need to sound legal. It needs to sound medically specific.

If the claim is denied

Start with the denial reason, not your frustration. Read the letter and match it against the chart, transfer notes, and policy language.

Then build the appeal around missing support. That may mean a stronger physician letter, a clarification from the receiving hospital, or records that show why the transfer met the plan's own standard. Families who need a practical framework can use these strategies for appealing medical claim denials from One For All Medical Billing to organize the next steps.

The strongest appeals don't repeat that the flight was important. They prove that the flight met the policy's conditions.

Questions from Families and Case Managers

Will my regular health insurance bring my loved one home

Usually, not just because you want that outcome. Health coverage may support a medically necessary transfer, but “home” and “covered destination” are not automatically the same thing. The key question is whether the destination is clinically necessary and supported in the records.

What should I do first when I get the hospital call

Get the basics in one pass. Ask for the hospital name, unit, attending physician, diagnosis as currently understood, and whether transfer has already been discussed. Then identify who holds the policy information and who can speak for the patient.

After that, focus on the chart. If the doctors haven't documented why transfer is needed, coverage discussions are premature.

Can a stable patient use something other than an air ambulance

Often, yes. Some patients don't need ICU-level aviation medicine. They may qualify for a medical escort on a commercial flight or another lower-acuity option. That decision should come from the patient's condition, oxygen needs, monitoring needs, mobility, and risk during boarding and flight.

What do case managers need from families to avoid delays

Families help most when they appoint one decision-maker, gather insurance details quickly, and avoid giving conflicting destination instructions. A case can stall when three relatives call with three different hospitals in mind.

What if the patient is bariatric or otherwise hard to transport

Say it early. Equipment, aircraft configuration, runway planning, ground ambulance selection, and crew setup all change when a patient has specialized size, mobility, or support needs. Waiting to disclose those factors creates preventable delays and mismatched quotes.

Does having medical flight insurance guarantee payment

No. It improves your position, but it doesn't erase the need for documentation, authorization, and policy fit. The phrase I come back to most is simple: coverage begins with clinical proof.

When families understand that early, they ask better questions, gather better records, and make better transport decisions. That's usually the difference between a chaotic transfer and a coordinated one.

If you're evaluating a possible transfer, start with the medical record, the receiving hospital, and the exact policy trigger. In medical flight cases, the flight itself is only part of the job. The documentation is what gets the case moving.