A call like this usually comes without warning. Your mother is in a hospital several states away after a fall. Your spouse got sick while traveling. A doctor says, “She may need transfer to another facility,” and suddenly you're trying to understand aircraft, ambulance coverage, prior authorization, and bills while also worrying about someone you love.

That's where families get stuck. They assume emergency care and emergency transport are the same thing. They aren't. A hospital can stabilize a patient, but moving that patient to the right hospital, or back closer to home, is a separate clinical and insurance process.

Emergency medical transport insurance sits in that gap. It can help pay for medically necessary transportation by ground or air, but only when the facts, paperwork, destination, and timing all line up with the policy. If you understand that operational side early, you can avoid the most common mistakes families make in a crisis.

What Is Emergency Medical Transport Insurance and Why It Matters

Emergency medical transport insurance is coverage for the medical movement of a patient when ordinary travel isn't safe. That might mean a ground ambulance, an air ambulance, or a medically supervised transfer between facilities.

The reason it matters is simple. Transport can become one of the biggest costs in an emergency. Medicare Part B generally covers 80% of the approved amount for ambulance services, leaving the patient responsible for the remaining 20% plus any deductible unless they have supplemental coverage. And the bills can be substantial. A 2022 analysis cited by Emergency Assistance Plus reported an average billed amount of about $51,300 for air ambulance services versus about $1,740 for ground transport.

The problem most families discover too late

Families often think, “We have insurance, so transport is covered.” Sometimes it is. Sometimes only part of it is. Sometimes the patient is covered for emergency treatment at the local hospital, but not for transfer to a preferred hospital or return home.

That distinction changes everything.

A doctor may decide a patient needs a higher level of care. The transport team may agree. But the insurer still wants to know questions like these:

- Was the transfer medically necessary

- What level of transport was required

- Why couldn't the patient travel another way

- Which destination qualified under the policy

- Who arranged the transport

Practical rule: The medical need for transport and the insurance approval for transport are related, but they are not the same step.

Who usually needs to think about this most

Some readers need this coverage more urgently than others:

- Travelers: A medical event away from home can trigger local treatment, transfer needs, and return-home questions all at once.

- Seniors: Medicare coverage rules can leave meaningful cost-sharing.

- Medically fragile patients: A stable patient may still need oxygen, monitoring, a stretcher, or a clinical escort.

- Families managing interfacility transfer: A local hospital may not offer the specialist or bed the patient needs.

If you're asking, “Do I need emergency medical transport insurance if I already have health insurance?” the honest answer is that many families only realize the gap when a transfer is already being discussed. By then, every hour feels shorter, and every decision feels more expensive.

What Emergency Medical Transport Insurance Actually Covers

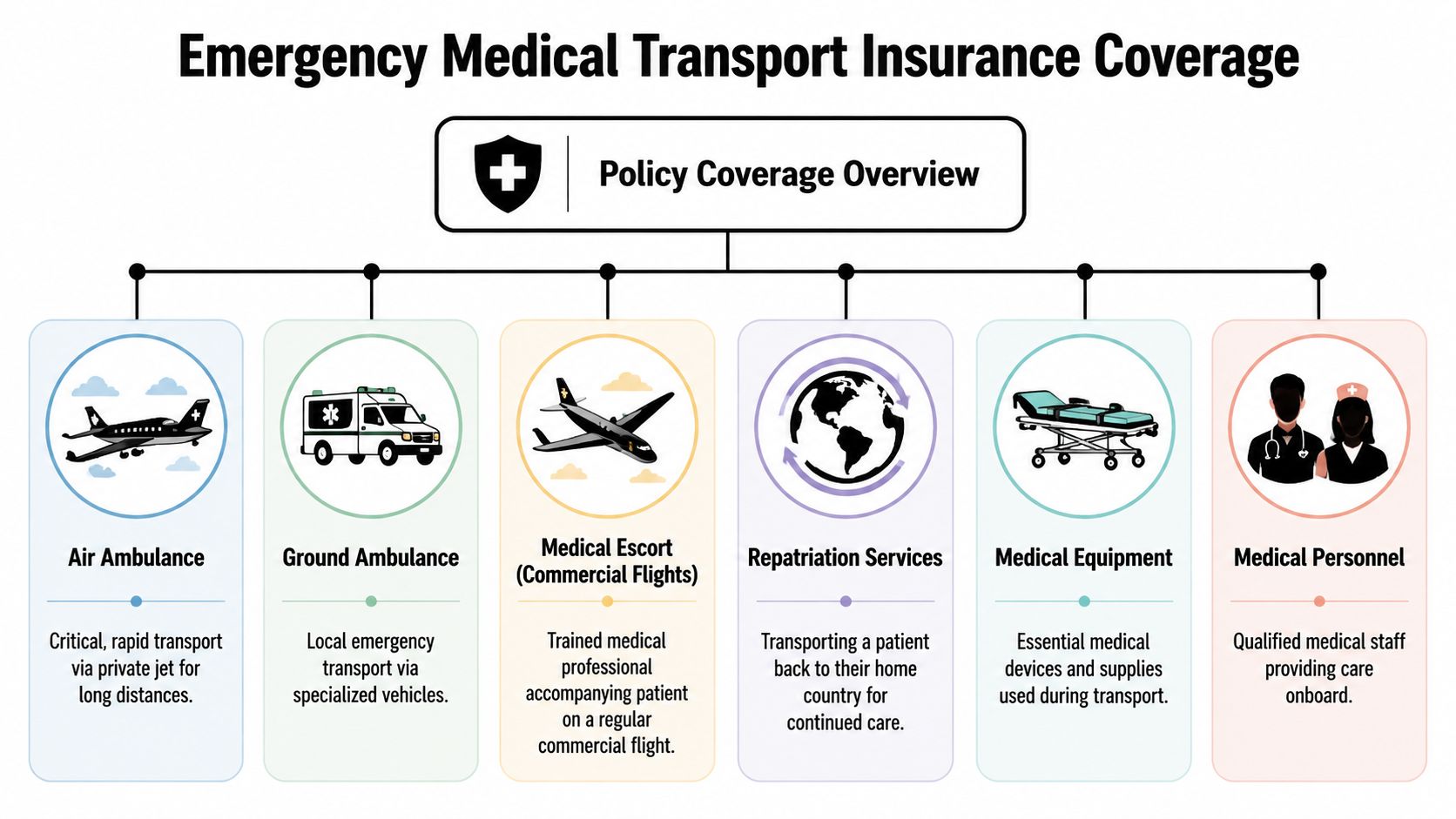

Coverage works best when you think of it as a set of tools. Different medical situations require different transport methods. The policy may cover some of them, all of them, or only under narrow conditions.

The main transport categories

Here's how families usually encounter them in real life:

| Transport type | When it's used | What families should ask |

|---|---|---|

| Ground ambulance | Local emergency response or shorter transfer | Is this emergency response, scheduled transfer, or discharge transport? |

| Air ambulance | Long-distance or time-sensitive transfer with onboard clinical care | Is air transport medically necessary or simply preferred? |

| Medical escort on a commercial flight | Patient is stable enough to fly commercially but still needs supervision | Will the insurer classify this as covered medical transport or ordinary travel assistance? |

| Specialized transport | Bariatric, stretcher, oxygen, cardiac monitoring, or other clinical needs | What exact level of care is being authorized? |

| Repatriation or transport home | Return closer to home after stabilization | Does the policy promise return home, or only transfer to an appropriate local facility? |

One question cuts through most confusion: Where will the patient be taken?

Nearest appropriate facility is not the same as home

Many travel-related plans cover transport only to the nearest appropriate facility, and they often require the insurer or assistance team to arrange the transport in advance, as explained by Allianz Travel Insurance's description of emergency medical transportation benefits. That means a patient may be moved to the closest hospital that can treat the condition, not to the hospital near home that the family prefers.

Many readers often ask, “Does emergency medical transport insurance bring you back home?” Sometimes, but not automatically.

If a policy says “nearest appropriate facility,” read that as a medical destination rule, not a family convenience rule.

That's also why it helps to compare transport-specific explanations like this overview of whether insurance covers air ambulance. It helps clarify the difference between emergency evacuation, medically supervised transfer, and return transport.

What may be part of the transport itself

Coverage may involve more than the vehicle. The transport episode can include:

- Medical crew: Nurses, paramedics, respiratory support, or other clinicians based on patient condition.

- Equipment: Monitoring, oxygen, stretcher support, and other gear needed during transfer.

- Care coordination: Communication between the sending hospital, receiving hospital, insurer, and transport dispatch.

- Ground segments: The patient may need ambulance support before and after a flight.

Families often focus on the aircraft because it's visible and dramatic. The insurer often focuses on the documentation behind it.

Reading the Fine Print Common Exclusions and Policy Limits

A transport policy is a contract. In a crisis, you don't need legal language. You need to know what can stop payment.

Three phrases that drive most disputes

Medical necessity means the insurer believes the patient required that level of transport for clinical reasons, not just convenience or preference.

Preauthorization means the insurer or assistance company wanted notice and approval before the trip, when the policy requires it.

Geographic limitations tell you where the policy works and whether cross-state or international movement changes the benefit.

Those phrases sound routine. They decide real money.

A 2024 actuarial white paper reported an average $643 balance bill per medical ground transportation service, which shows how patient liability can remain even when transport occurs and even when some coverage is available, according to the MASA special report on emergency medical transport costs.

Common places coverage breaks down

Families should scan for these issues before they assume a trip is covered:

- Out-of-network transport providers: A medically necessary trip can still generate unexpected patient responsibility.

- Non-emergent reclassification: The insurer may later argue the patient could have traveled by a less intensive method.

- Unapproved destination: The patient was moved to a preferred hospital rather than the covered destination.

- Failure to use the insurer's dispatch process: This is especially important in travel-related transport benefits.

- Condition-based exclusions: Policies may place limits around pre-existing conditions or travel that conflicts with medical advice.

- Companion expectations: Family seating, pet transport, or non-medical add-ons may not be included.

What to review before saying yes

Use this short document check when transport is being discussed:

| Policy item | Why it matters |

|---|---|

| Definition of covered transport | Tells you whether the plan is paying for emergency evacuation, interfacility transfer, or both |

| Destination rules | Determines whether transport ends at the closest capable hospital or can continue farther |

| Authorization rules | Shows whether advance approval is required |

| Network language | Affects patient billing exposure |

| Appeal process | Matters if the claim is reduced or denied |

If the family can ask only one billing question, ask this: “What part of this trip could still become the patient's responsibility?”

How to Coordinate Medical Transport from First Call to Arrival

When a transfer is being considered, the cleanest process is the one everyone follows early. Families feel less overwhelmed when each party has a job.

Early in the process, it helps to visualize the chain of events.

The seven-step workflow families can follow

Start with the current care team

Ask the sending physician or case manager whether the patient needs emergency transfer, urgent interfacility transfer, or a medically supervised but stable transport. Those are not interchangeable.Confirm the receiving facility

A transfer can't move forward cleanly without destination acceptance. Someone at the receiving hospital must agree to take the patient and confirm the needed service line or bed.Call the insurer or assistance company immediately

Don't wait until the transport is booked. Ask whether they must arrange the transport themselves, whether prior authorization is required, and what level of transport they're willing to review. Families who want a clearer sense of the approval process can review this explanation of medical transport prior authorization.Match the transport level to the patient's condition

A stable patient who still needs clinical supervision may qualify for a different service than a critical care air ambulance. The key issue is often not whether insurance exists, but what documentation, destination, and level-of-care criteria support payment for a medically supervised transfer rather than non-covered transportation, as discussed in SafeRide Health's overview of NEMT-related transport questions.

What the hospital needs to gather

The transport team and insurer usually need a packet that answers practical questions fast.

- Clinical summary: Current diagnosis, reason for transfer, and why the current facility can't provide the needed care.

- Transport justification: Why wheelchair, private car, or ordinary travel isn't safe.

- Recent records: Notes, medication list, oxygen needs, imaging summary, and current orders.

- Accepting physician details: The receiving doctor and hospital unit.

- Patient logistics: Weight, mobility limits, infection precautions, and companion questions if permitted.

The smoother transfers usually aren't the ones with the least urgency. They're the ones with the clearest paperwork.

Later in the process, this short video can help families understand the rhythm of medical transport coordination:

Who does what during the handoff

A lot of conflict happens because families assume one party is handling a task that belongs to someone else.

| Party | Main responsibility |

|---|---|

| Sending hospital | Stabilizes patient, documents need, prepares records |

| Receiving hospital | Accepts patient and confirms destination |

| Insurer or assistance company | Reviews benefit rules, authorization, and vendor requirements |

| Transport provider | Confirms clinical capability, timing, crew, and movement plan |

| Family | Consents, shares insurance details, tracks names and decisions |

Ask for names every time you speak with someone. In a transfer, verbal promises disappear quickly unless someone can tie them to a person, date, and time.

Navigating Bills and Submitting a Successful Claim

Once the patient arrives, many families exhale too early. The transport may be over. The financial file is just beginning.

What to save before paperwork scatters

Keep one folder, digital or paper, with everything tied to the trip:

- Insurance authorization notes: Names, reference numbers, call dates, and what each representative said.

- Transport paperwork: Consent forms, dispatch confirmation, and provider details.

- Medical records: Sending hospital notes, physician transfer order, receiving hospital acceptance, discharge summary.

- Bills: Itemized invoices, not just balance statements.

- Proof of medical necessity: Any record that explains why this transport method was required.

If your records are incomplete, a simple framework like FaxZen's medical records guide can help families request the right documentation without guessing what the hospital release form should include.

A practical claim approach

Do these things in order:

- Submit the itemized bill first: A one-line statement rarely tells the insurer enough.

- Attach the transfer rationale: Make it easy for the reviewer to see why lower-acuity transport wasn't appropriate.

- Add destination proof: Include the acceptance details from the receiving facility if the transfer was hospital-to-hospital.

- Respond quickly to requests: Claims often stall because the insurer asks for one additional note and no one realizes it.

- Escalate calmly when needed: Ask for the denial reason in writing and match your appeal to that exact issue.

Keep this in mind: A clean appeal answers the insurer's stated reason for denial. It doesn't just repeat that the situation felt urgent.

Medicaid questions need special attention

For Medicaid families, transport rules can be confusing because the federal framework treats transportation assurance as a program-level obligation, not a separate emergency-transport category. Federal guidance says states must ensure access to both emergency and non-emergency medical transport under Medicaid rules, as outlined in the Medicaid transportation assurance guidance.

That means your billing path may depend heavily on the state program structure, medical-necessity documentation, and whether the trip was processed through the right channel. If someone tells you “Medicaid covers transport,” your follow-up question should be, “Under which process, and what records do you need from us?”

How to Choose a Medical Transport Provider

Sometimes the insurer chooses the vendor. Sometimes the hospital presents options. Sometimes the family is arranging a private-pay transfer and has to evaluate providers quickly.

That's not the moment to ask only, “How soon can you fly?” You also need to ask, “Can you safely handle this patient's exact condition?”

A better provider checklist

Use questions like these:

- Clinical capability: What types of patients can your crew manage during flight or long-distance transfer?

- Transport modes: Do you arrange only air ambulance, or also ground legs and medical escorts?

- Operational coordination: Will your team work directly with both hospitals on records, timing, and handoff details?

- Family logistics: Can a family member accompany the patient if clinically appropriate?

- Special situations: Can you handle bariatric transport, oxygen needs, or stretcher-based movement?

- Communication style: Who updates the family when plans change?

Compare the service model, not just the vehicle

Some providers operate only a single part of the chain. Others coordinate the full trip from bedside to bedside. For many families, that difference matters more than the aircraft name.

One example to evaluate is Med Jets by Air Trek's emergency medical transport services, which include emergency medical flights, medical escorts, and ground coordination. That kind of end-to-end model can be useful when the case involves multiple handoffs rather than a simple airport-to-airport movement.

Ask the provider to explain the trip in sequence. If they can't describe the bedside handoff, the receiving facility coordination, and the paperwork flow, keep asking questions.

The best choice is usually the provider whose clinical scope, communication process, and coordination style fit the patient in front of you.

Your Emergency Medical Transport Checklist and FAQs

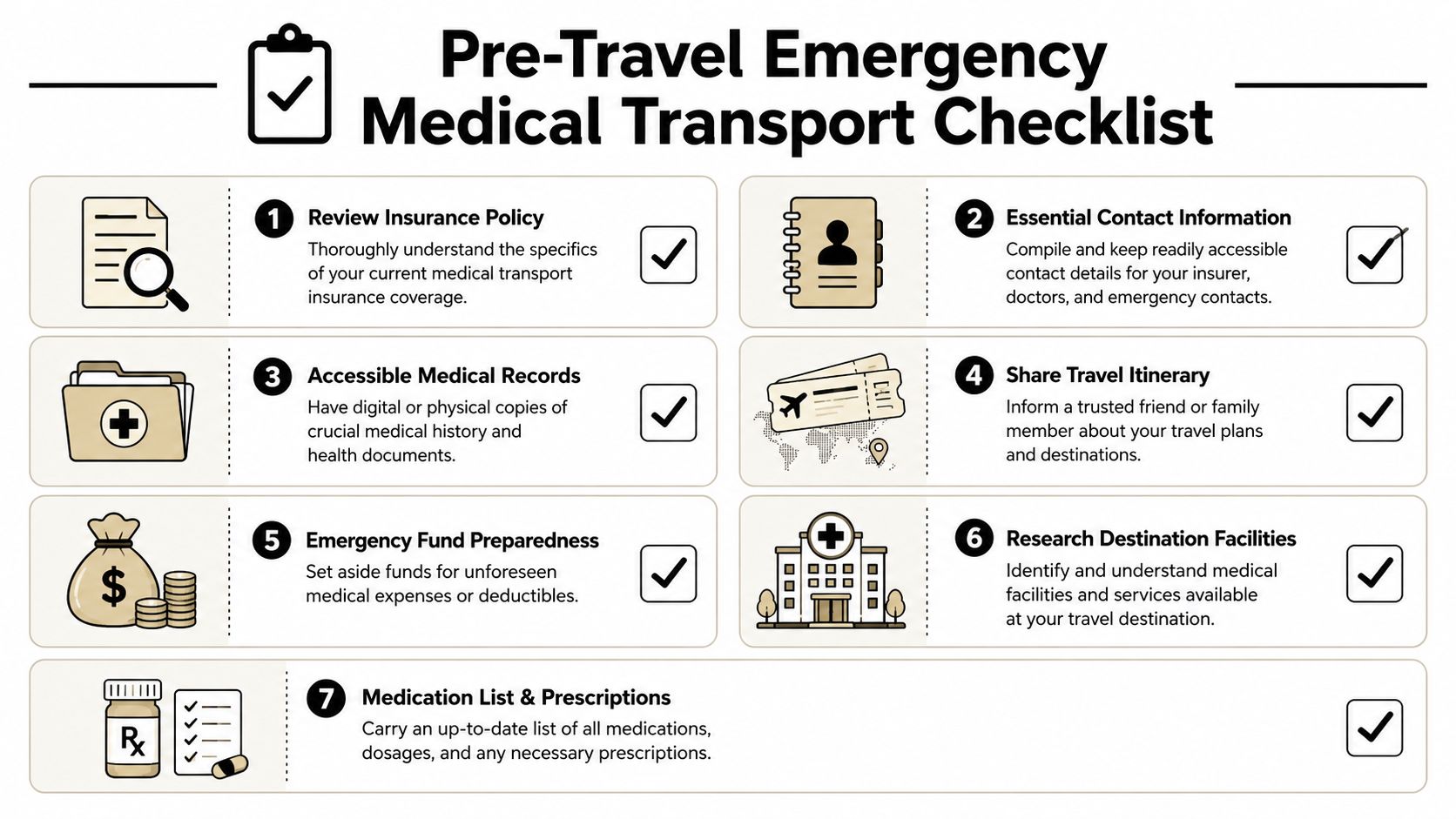

When families prepare in advance, they make better decisions under stress. You don't need to memorize policy language. You need a short readiness routine.

Pre-travel and pre-crisis checklist

- Review your policy wording: Look for destination rules, authorization requirements, and excluded scenarios.

- Save the assistance phone number: Don't assume you can find it quickly during an emergency.

- Carry a current medication list: Include diagnoses, allergies, and treating physicians.

- Keep records accessible: A phone folder or printed packet can save hours.

- Tell family where your documents are: Someone else may need to act for you.

- Know your likely hospitals: If you travel often, identify larger facilities in the area.

- Ask one hard question before buying: “Does this policy cover medically necessary transport home, or only to the nearest appropriate facility?”

Frequently asked questions

Does regular health insurance cover emergency medical transport insurance needs?

Sometimes partly, sometimes narrowly. Coverage may depend on medical necessity, destination, network status, and who arranged the trip.

Can I choose my destination hospital?

Not always. Some policies tie coverage to the nearest appropriate facility rather than the hospital the family prefers.

What if the patient is stable but still can't travel alone?

That's where medically supervised transfer, stretcher transport, or a medical escort may become relevant. The chart needs to show why ordinary travel wasn't safe.

What if a claim is denied?

Get the denial reason in writing, gather the missing records, and appeal to that specific reason. Broad appeals are weaker than targeted ones.

What's the biggest mistake families make?

They arrange transport first and verify benefit rules second.

Emergency medical transport insurance is most useful when you treat it as both a coverage product and a coordination process. The policy matters. The paperwork matters. The destination matters. In a crisis, the family that asks clear questions early usually has a smoother path.