A hospital calls late in the day. A patient is stable enough to move, but not stable enough to ride home in a family car. The family wants to know one thing first: “Will insurance cover this?” The discharge team asks a different version of the same question: “What level of transport can we justify, authorize, and get paid?”

Those questions sound simple. They rarely are.

Medical transport insurance coverage sits at the intersection of clinical need, payer rules, network contracts, and paperwork. A trip can be medically appropriate and still denied. A flight can be “covered” and still leave the patient with a painful bill. A family can do everything right, then learn that the wrong transport mode was chosen or pre-authorization was missed.

That's why families and case managers need a practical approach, not vague advice to “check the policy.” The essential work is identifying which payer's rules apply, matching the transport mode to the patient's condition, and documenting the decision in a way that survives payer review. When transport gets expensive, the stakes rise fast. A 2024 report estimated average allowed amounts at about $1,740 for ground medical transport and about $51,300 for air medical transport in 2022, according to the MASA Assist emergency medical transport cost report.

Your Guide to Navigating Medical Transport

A common scenario goes like this. A loved one is hospitalized far from home after surgery, a cardiac event, or a fall. The doctors say the patient can transfer to another facility or return closer to family, but only with medical supervision. The family assumes insurance will step in because the need is obvious. Then the questions start. Ground or air? Emergency or non-emergency? In-network or out-of-network? Does Medicare apply, or a Medicare Advantage plan, or Medicaid, or a private policy through work?

That confusion is normal. It happens because transport coverage isn't based on one simple yes-or-no rule. It depends on who the payer is, whether the transport is medically necessary, what level of service is justified, whether authorization is required, and whether the provider meets billing and participation requirements.

What usually goes wrong

Families often focus on the trip itself. Payers focus on the file.

A payer reviewer usually asks a narrower set of questions:

- Was the transport medically necessary: Could the patient safely travel another way?

- Was the mode correct: Did the patient need a wheelchair van, stretcher, BLS ambulance, or critical care transport?

- Was approval obtained first: If the plan requires pre-authorization, was it secured?

- Was the provider billable under the plan: Network and participation rules matter.

Practical rule: Medical transport claims are won or lost on clinical documentation and payer process, not on how urgent the situation felt to the family.

The path that works

When a transport goes smoothly, the team does three things early. They identify the payer, they define the patient's transport limitations in clinical terms, and they coordinate directly with the transport provider before the trip happens.

That doesn't remove every risk. It does prevent the most expensive misunderstandings.

Decoding Your Coverage Source and Its Rules

The same patient trip can be treated very differently depending on the payer. I usually describe it as three different rulebooks for the same game. The destination may be identical, but the approval standards, billing mechanics, and patient cost exposure aren't.

Medical Transport Coverage at a Glance by Payer

| Payer Type | Primary Driver | Typical Coverage for Air Ambulance | Key Consideration |

|---|---|---|---|

| Private insurance | Contract terms and utilization review | Often tied to medical necessity, authorization, and network status | Check plan-specific exclusions, prior approval rules, and balance billing risk |

| Original Medicare | Federal coverage rules | Generally limited to cases where other transportation would endanger the patient's health | Routine non-emergency transport usually isn't covered the same way |

| Medicaid | Federal access requirement with state administration | Depends on state administration and medical necessity | State-specific rules can change eligibility, trip approval, and billing methods |

Private insurance means contract rules

Commercial plans usually give the most room for variation. One private plan may cover a medically necessary transfer if the provider obtains pre-authorization and uses an approved carrier. Another may limit payment, classify the service at a lower level, or deny out-of-network charges even when the clinical need is real.

This matters in accident cases too. If a transport claim intersects with auto coverage, state-specific rules can affect which payer should be billed first. For Florida readers, Haddad & Associates P.A. explains how Florida PIP works in a way that helps families understand when auto insurance may enter the picture.

Medicare means federal standards, then plan variation

Original Medicare generally does not cover routine non-emergency transportation, while many Medicare Advantage plans now include transportation benefits, often with 12 to 48 one-way trips per year, according to eHealth's Medicare transportation overview. That's a major practical difference for seniors.

The trouble is that people hear “Medicare” and assume one set of rules. There isn't one set anymore in practice. Original Medicare, Medicare Advantage, and supplemental coverage can all change the answer. For readers sorting out higher-acuity flights specifically, this guide on whether Medicare covers air ambulance is a useful starting point.

Medicare questions usually fail when the team verifies the patient's card, but not the actual plan structure behind it.

Medicaid means access, but state administration

Medicaid approaches transport from an access-to-care perspective. Under federal law, state Medicaid plans are required to assure necessary transportation for beneficiaries. That makes transport a core access mechanism, not a fringe extra. At the same time, states retain broad discretion in how they administer that benefit, so authorization steps, vendor rules, and documentation expectations can differ materially from one state to another.

For discharge planners, that's the point to remember. “It's Medicaid” doesn't tell you enough. You still need the state-specific rulebook.

The Golden Rule of Medical Necessity

Every transport claim turns on one gatekeeper concept: medical necessity. Not convenience. Not family preference. Not distance from home. The payer asks whether the patient's condition made ordinary transportation unsafe and whether the selected transport mode was the least intensive option that still protected the patient.

That second part is where many denials happen. Payers frequently deny claims if a lower-acuity option could have safely met the patient's needs, as reflected in CMS guidance on transportation assurance and medical necessity.

What covered documentation looks like

Strong documentation ties the patient's condition to the transport level.

For example, a stretcher trip may be supportable when the patient cannot sit upright for the duration, needs positioning, or has mobility and safety limitations that make wheelchair transport inappropriate. A higher-acuity ambulance trip may be supportable when the patient requires ongoing monitoring, oxygen management, or clinical intervention during movement between facilities.

For air transport, the file has to answer a harder question. Why couldn't ground transport do the job safely within the patient's clinical window?

What weak documentation looks like

Weak charts use broad statements such as “patient needs transport assistance” or “family requested transfer.” Those statements may be true, but they don't establish payable medical necessity.

A payer wants the specifics:

- Functional limits: Can the patient sit, transfer, or tolerate travel time?

- Clinical monitoring needs: What must be monitored en route?

- Risk of deterioration: What could go wrong if the patient used a lower level of transport?

- Mode selection rationale: Why is this level the least costly safe option?

If the chart doesn't explain why a cheaper mode was unsafe, the payer may decide the expensive mode was optional.

The question families should ask

When families ask whether insurance covers air ambulance, I suggest they ask a more useful question first: “What exactly in the patient's condition prevents safe ground transport?” That question pushes the team toward the clinical facts that matter.

This resource on whether insurance covers air ambulance helps frame that distinction clearly. The trip itself doesn't trigger coverage. The patient's inability to travel safely by ordinary means does.

Understanding In-Network vs Out-of-Network Costs

A transport can be medically necessary and still become a financial shock. That's the part families often find hardest to accept. They hear “approved” and think “fully paid.” Those are not the same thing.

Why network status matters so much

In transport, especially air transport, provider availability is often limited. Families may not have a true menu of in-network choices at the moment a transfer is being arranged. Even so, network status can determine whether the insurer pays under negotiated terms or leaves the patient exposed to a much larger balance.

The practical issue isn't only whether the service is covered. It's also whether the carrier is contracted, whether the allowed amount is capped, and whether the provider can bill the patient for the difference.

Neutral consumer guidance from the NAIC notes that even when air transport is medically necessary, patients can still face substantial out-of-pocket bills. Air ambulance services often average $12,000 to $25,000 per flight, and those gaps can result from out-of-network status, deductibles, and policy limits, as explained in the NAIC overview of air ambulance coverage.

Why “covered” can still mean “you owe”

Here's the common misunderstanding. A plan may acknowledge the claim, apply coverage rules, and still leave the patient with a large bill because only part of the charge is treated as payable under the policy.

That's why it helps to understand the basic difference between contracted and non-contracted care before the trip is scheduled. This guide to your rights with network providers gives a plain-language explanation of the network issues families run into across health plans.

For a broader look at how ambulance billing interacts with medical insurance, this article on whether medical insurance covers ambulance transport is also worth reviewing.

A quick explainer can help before you sign anything:

Questions to ask before transport is booked

- Is the provider in-network for this specific plan: Don't assume based on a hospital relationship.

- If out-of-network, what part of the bill might fall to the patient: Ask before launch, not after.

- Is prior authorization tied to a specific carrier or aircraft type: Some plans care about both.

- Will the insurer discuss a single-case agreement: In unusual transfers, that can matter.

The most expensive transport problem is not always denial. Sometimes it's partial payment.

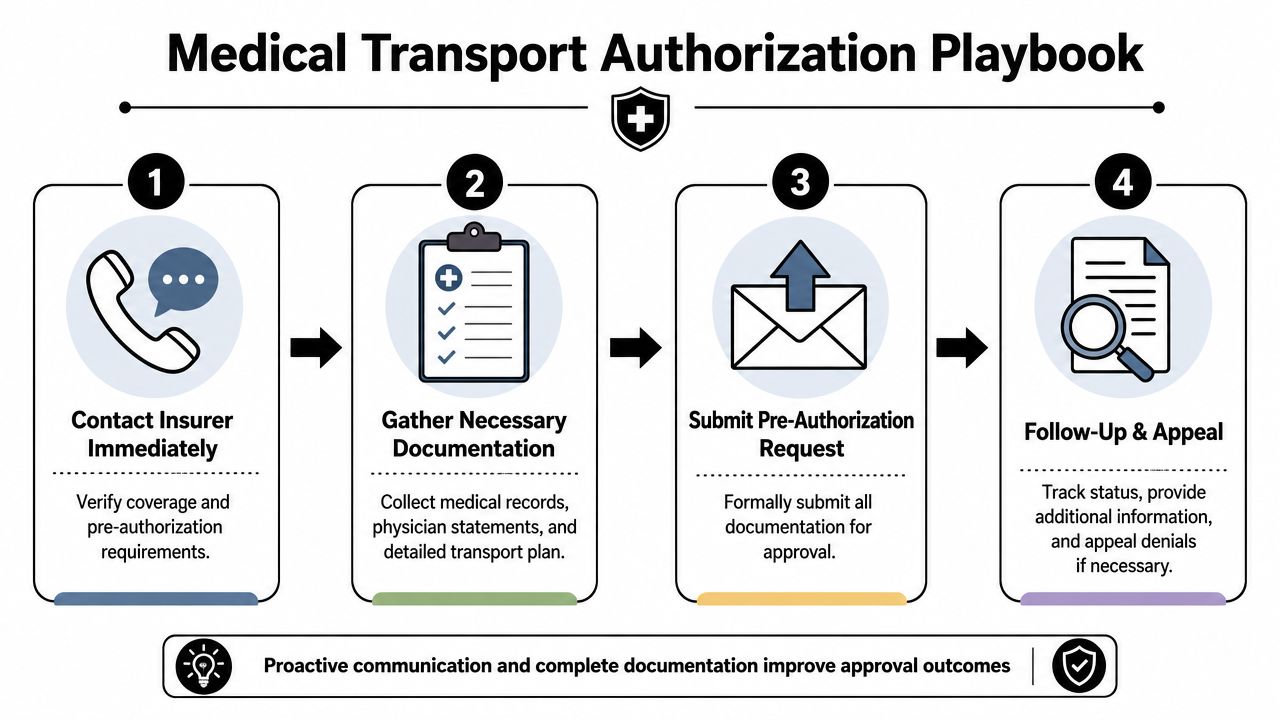

The Authorization and Documentation Playbook

Most avoidable denials happen before the wheels move. The right playbook is simple, but it has to happen in sequence and it has to happen fast.

Step one is benefit verification

Call the payer early, before anyone promises a transport mode to the family. Confirm the patient's active coverage, whether the trip is being treated as emergency or non-emergency transport, whether pre-authorization is required, and whether the insurer requires use of a contracted provider.

For Medicaid cases, this front-end work is especially important. Federal law requires state plans to assure necessary transportation for beneficiaries, which has made authorization and documentation central to access for millions of enrollees, as described in the Medicaid assurance of transportation guidance.

Step two is building the clinical file

The physician order alone often isn't enough. The chart needs a clean narrative that explains why the patient cannot use a lower-acuity mode safely. That may include progress notes, oxygen needs, mobility limits, monitoring requirements, transfer risks, and a physician certification or equivalent form when required by the payer.

When hospitals move this paperwork by fax, process matters. Teams that haven't updated their workflow should review practical guidance on implementing HIPAA-compliant faxing, because transport authorizations often fail on missing pages, illegible records, or delayed transmission between case management, nursing, and the insurer.

Step three is submitting the right request

A good authorization request is not a stack of random records. It is a curated packet that makes the payer reviewer's job easy.

Include, at minimum:

- The transport order with the requested mode.

- A concise clinical summary that states why lower-acuity transport is unsafe.

- Supporting records that match the summary.

- Facility details for sending and receiving locations.

- Provider information for the transport company and any network identifiers if applicable.

Step four is active follow-up

Silence from the payer is not approval. Someone needs to track the request, answer follow-up questions, and document every call, reference number, and name.

Experienced coordinators provide significant value. A transport coordinator can gather records, align the requested mode with the patient's condition, and keep hospital staff, payer staff, and family on the same page. Providers such as Med Jets by Air Trek handle air ambulance, medical escort, and ground coordination, which can help when the issue isn't just flying the patient but also managing documentation and handoffs across multiple parties.

How to Handle Claim Denials and Appeals

A denial is frustrating, but it isn't the end of the case. Many transport denials come down to documentation gaps, authorization disputes, or payer disagreement about the service level. Those are all issues you can challenge.

Start with the denial reason, not your frustration

Read the explanation carefully. Most denials fall into a few categories:

- Not medically necessary: The payer believes a lower-acuity mode would have been safe.

- Authorization missing or late: The payer says required approval wasn't obtained.

- Incorrect level of service: The reviewer agrees transport was needed, but not at the billed level.

- Provider or billing issue: Credentials, network participation, or claim coding created the problem.

Each denial reason requires a different response. A generic appeal letter rarely works.

Build the appeal around the payer's own issue

If the denial says “not medically necessary,” the appeal should not spend two pages describing how stressed the family was. It should show, in clinical terms, why the patient could not safely use the lower level of transport the payer says was available.

That often means adding:

- A physician letter that directly addresses the denied mode question

- Nursing or therapy notes showing transfer limits or monitoring needs

- Timeline details showing why delay or alternate transport would have created risk

- Any authorization records if the insurer's file is incomplete

Appeals work best when they answer the exact denial language line by line.

Don't ignore the billing side

Sometimes you won't overturn the whole denial, especially in out-of-network cases. That doesn't mean the bill is fixed in stone.

Ask the provider's billing team whether they will review the balance, rebill with additional records, or negotiate after an underpayment. If the insurer treated the service as partially covered, request a full explanation of how the allowed amount was calculated and whether a separate internal review is available for payment level, not just coverage.

Use every level of review available

Most plans offer an internal appeal first. Many cases can also move to an external review depending on the plan type and issue involved. Keep copies of everything. Document call dates, upload confirmations, and fax receipts. If records were sent, prove they were sent.

Families often feel powerless at this stage. They aren't. The strongest appeals are organized, specific, and clinically focused. The weakest appeals say only that the bill feels unfair.

Conclusion Partnering for a Smooth and Safe Journey

Medical transport insurance coverage gets easier to manage when you stop treating it like a mystery and start treating it like a process. First identify the payer rulebook. Then match the transport mode to the patient's actual condition. Then make sure the documentation tells that story clearly enough for a reviewer who never met the patient.

That's the core lesson. Coverage depends less on how serious the situation feels and more on whether the file proves the right facts in the right format. Medical necessity is the hinge. Authorization is the checkpoint. Network status and billing terms shape what the family may still owe.

For hospital case managers, that means slowing down just enough to verify benefits, confirm the requested level of service, and send a complete packet. For families, it means asking sharper questions before transport is booked. Who is the payer? Is this provider in-network? What exactly makes this mode medically necessary? Was approval obtained?

The transport itself may be urgent. The decisions around it still need discipline.

If you're arranging a complex transfer and want help coordinating the clinical, logistical, and insurance pieces, contact the team at Med Jets by Air Trek. A seasoned coordinator can help you sort through the payer rules, move the records where they need to go, and reduce the risk of a preventable denial or surprise bill.