When a hospital says a loved one needs an air ambulance, the medical decision often happens fast. The financial paperwork does not. Families get a quote, a service agreement, and a request for signatures while they're also calling relatives, speaking with nurses, and trying to understand what happens next.

That's where confusion starts. A contract might mention deposits, guarantor responsibility, insurance assignment, late payment language, and cancellation terms all on the same page. Under stress, those clauses can feel harsher than they really are, or safer than they really are. Usually, they're neither. They're operational rules meant to make sure the aircraft, medical crew, and coordination work can move without delay.

This guide translates air ambulance payment terms and conditions into plain English. If you're a family member, case manager, or discharge planner, the goal is simple: know what you're agreeing to, know what questions to ask, and know where contract language stops and federal patient protections begin.

Your Guide to Medical Flight Financial Agreements

A family can go from discussing ventilator settings to signing a financial agreement in the span of one phone call. I see that shift catch people off guard all the time. The medical need feels urgent, but the contract still matters because it sets the billing rules before the aircraft ever lifts off.

An air medical financial agreement does more than confirm a price. It usually spells out who is financially responsible, whether insurance benefits are assigned to the transport company, whether a deposit is due, and what happens if the trip changes because of weather, clinical instability, or receiving-facility delays. In practice, it is the document that decides who gets billed first and who may still be asked to pay later.

Payment terms are the timing and conditions for payment. In an air ambulance setting, that can include prepayment, payment after the flight, insurer billing, guarantor liability, and deadlines if a balance remains. Some contracts also define refund rules, interest or collection costs, and what counts as a canceled mission versus a completed transport.

The part families miss most often is the gap between the contract and federal law. A signed agreement may say the patient or guarantor is responsible for any remaining balance. That language does not automatically override patient protections under the No Surprises Act. For many covered transports, the primary concern is not just what the contract says. The fundamental issue is whether the provider can legally bill beyond the patient cost-sharing amount allowed under federal rules.

That distinction matters.

I explain it this way: the contract is the company's billing document, but it does not erase rights the law gives the patient. If you are reviewing terms before a flight, it also helps to compare them with a separate medical flight insurance option. Insurance membership, health plan coverage, and contract liability can affect the same trip, but they are not interchangeable.

Read the agreement with a practical goal. Identify who is signing as guarantor, what charges may still be pursued after insurance, and whether the document says anything that seems broader than current federal balance-billing protections. In air ambulance cases, that last point is often the one that saves families from assuming they owe more than the law allows.

Decoding the Air Medical Transport Contract

At 2 a.m., a family member is on speakerphone, the sending hospital wants an answer, and a contract arrives by email with a signature line for the guarantor. In that moment, the fastest way to avoid a billing mistake is to sort out who is making the medical decision, who is arranging the flight, and who may later be asked to pay.

Who the main parties are

Air ambulance contracts usually involve four parties, and each one controls a different part of the process:

| Party | Role in the agreement | What to watch |

|---|---|---|

| Provider | Arranges and performs the medical transport | Scope of service, billing process, cancellation rules |

| Patient | Receives the service | Consent, insurance information, clinical eligibility |

| Guarantor | Accepts financial responsibility if balance remains | Personal liability, payment schedule, collections language |

| Insurer | May reimburse some or all eligible charges | Coverage limits, denials, preauthorization, medical necessity review |

The guarantor line deserves extra attention. Signing it usually means more than approving the transport. It can mean agreeing to cover charges the insurer does not pay, at least under the contract language.

That is the contract view. Federal law can change the billing result.

In air ambulance cases, families often assume the guarantor clause settles the whole question. It does not. A provider can write broad balance-due language into the agreement, but the No Surprises Act may still limit what the patient or guarantor can legally be billed for a covered transport. Read the contract and the legal protections side by side, not as if the contract automatically wins.

What standard payment language means here

Payment terms are the timing rules. They spell out whether money is due before the flight, after the flight, or in stages. They also usually state how payment can be made, when a balance becomes overdue, and whether collection costs or interest may be added if the account is not resolved.

In ordinary business billing, terms such as net 30 or cash on delivery mainly set expectations. In air medical transport, the same wording carries more weight because the provider is committing aircraft time, crew, fuel, medical equipment, and coordination with hospitals almost immediately. That is why these agreements often read more like a service commitment with financial backing than a simple invoice.

A separate issue often gets mixed into billing disputes. Insurance approval is not the same as private financial responsibility. If your team is still sorting out payer requirements, this guide to understanding prior authorization for medical transport helps explain how insurer approval fits into the process.

Practical rule: The contract identifies who the provider may bill. It does not decide the final amount legally owed if federal balance-billing protections apply.

That distinction saves families from agreeing with the first bill before checking whether the No Surprises Act limits it.

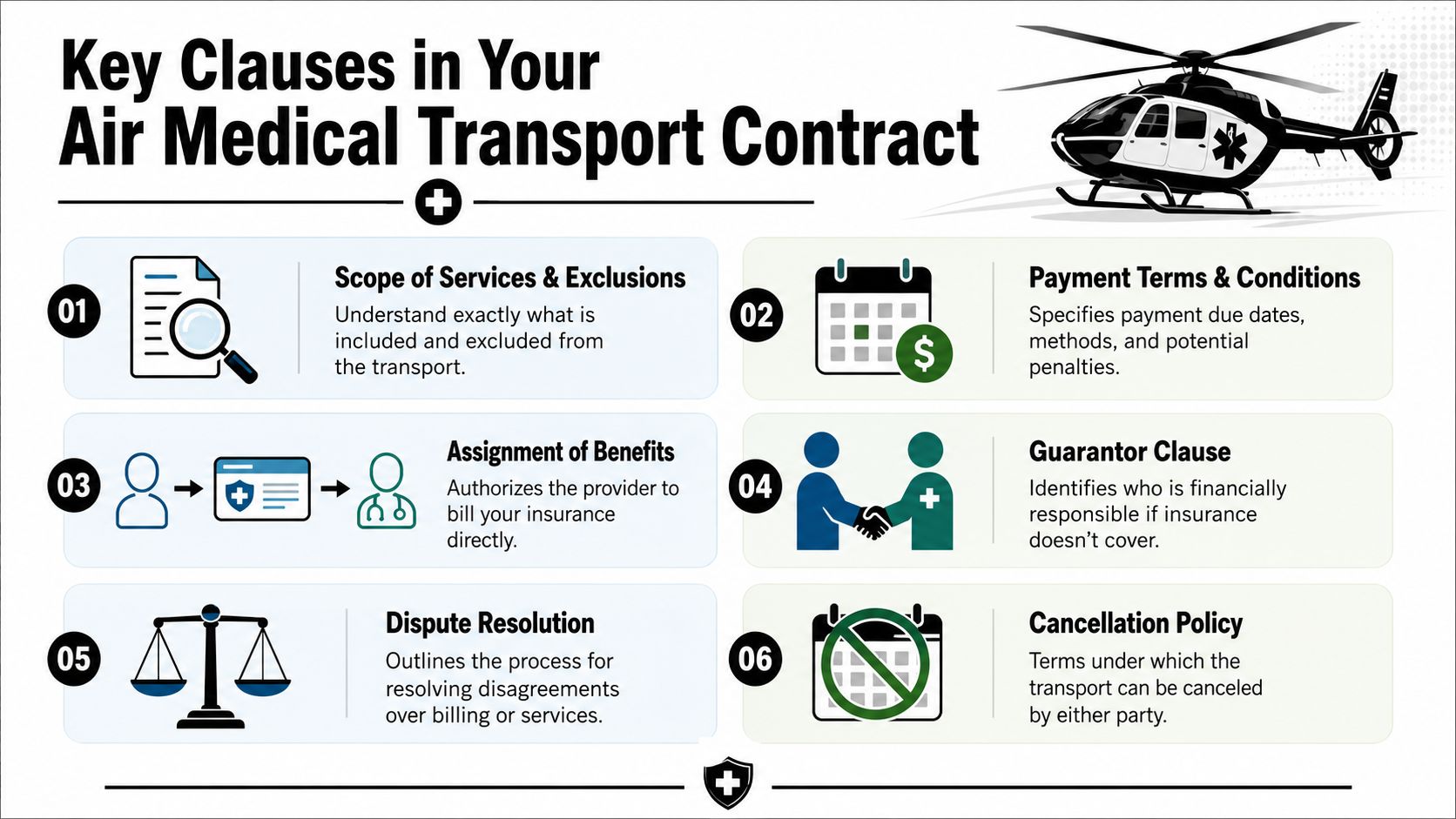

Key Clauses You Must Understand

The clauses below are the ones families circle, question, and sometimes misread. None of them exist by accident. Each serves a specific operational or financial purpose.

Deposit and advance payment

What it means

Some providers ask for payment before the aircraft launches, either in full or in part. In high-value medical transport, upfront requirements such as 50-100% advance are used to reduce nonpayment risk. Evidence indicates that companies using advance payment clauses reduce delinquency by about 40-60% compared with providers relying only on post-service billing.

Why it matters

From the provider's side, the largest costs begin immediately. The crew is activated, the aircraft is committed, and the transport slot may block out other missions. If the payer later disappears or insurance delays reimbursement, the financial hole opens right away.

“Advance payment language is not there to punish a family. It's there because the flight's cost starts before wheels-up.”

Sample wording you may see:

“Client agrees to remit required deposit prior to transport scheduling. Provider may delay non-emergent services until deposit is received.”

Cancellation and abort language

What it means

This clause explains what happens if the patient becomes too unstable to fly, the receiving facility changes plans, weather blocks the route, or the mission is canceled for another reason.

Why it matters

Families often assume cancellation means no charge. In practice, some costs may already have been incurred. A fair contract should say what counts as a refundable event, how fast any refund is processed, and what non-refundable costs may be deducted.

Look for these points:

- Medical instability definition so you know who decides the patient can't fly

- Weather cancellation rule so operational safety decisions are clearly separated from billing

- Standby cost treatment so there's no argument later about crew time or aircraft preparation

Assignment of benefits

What it means

This gives the provider permission to bill insurance directly and receive any covered reimbursement.

Why it matters

Without it, the insurer may send payment or paperwork through a slower route, which can stall claim handling. This clause usually helps both sides, but it does not erase guarantor liability unless the contract clearly says so.

Sample wording you may see:

“Patient and/or guarantor assigns insurance benefits to provider and authorizes direct payment where permitted.”

Balance billing and guarantor liability

What it means

This is the language that says the patient or guarantor remains responsible for amounts not paid by insurance.

Why it matters

This is often the most emotionally difficult clause because it sounds open-ended. The key is to separate two questions: what the contract says, and what the law allows in a given billing situation. A contract can state broad responsibility, but that doesn't always decide the final patient balance.

Check whether the clause:

- ties liability to all nonpaid amounts,

- limits liability to patient-responsibility amounts,

- or preserves room for insurance appeals and legal protections.

Dispute resolution and billing errors

What it means

This clause says how billing disagreements are handled. It may require written notice, internal review, mediation, or another dispute path.

Why it matters

Medical transport deals with multiple payers and moving paperwork. Contracts lacking a clear dispute-resolution clause can see a 35% increase in administrative overhead and a 25% delay in fund collection. That tells you something important: clear procedures help everyone, not just the provider.

A good clause should tell you where to send a dispute, what records to include, and whether payment is paused during review.

Navigating Insurance and Guarantor Responsibilities

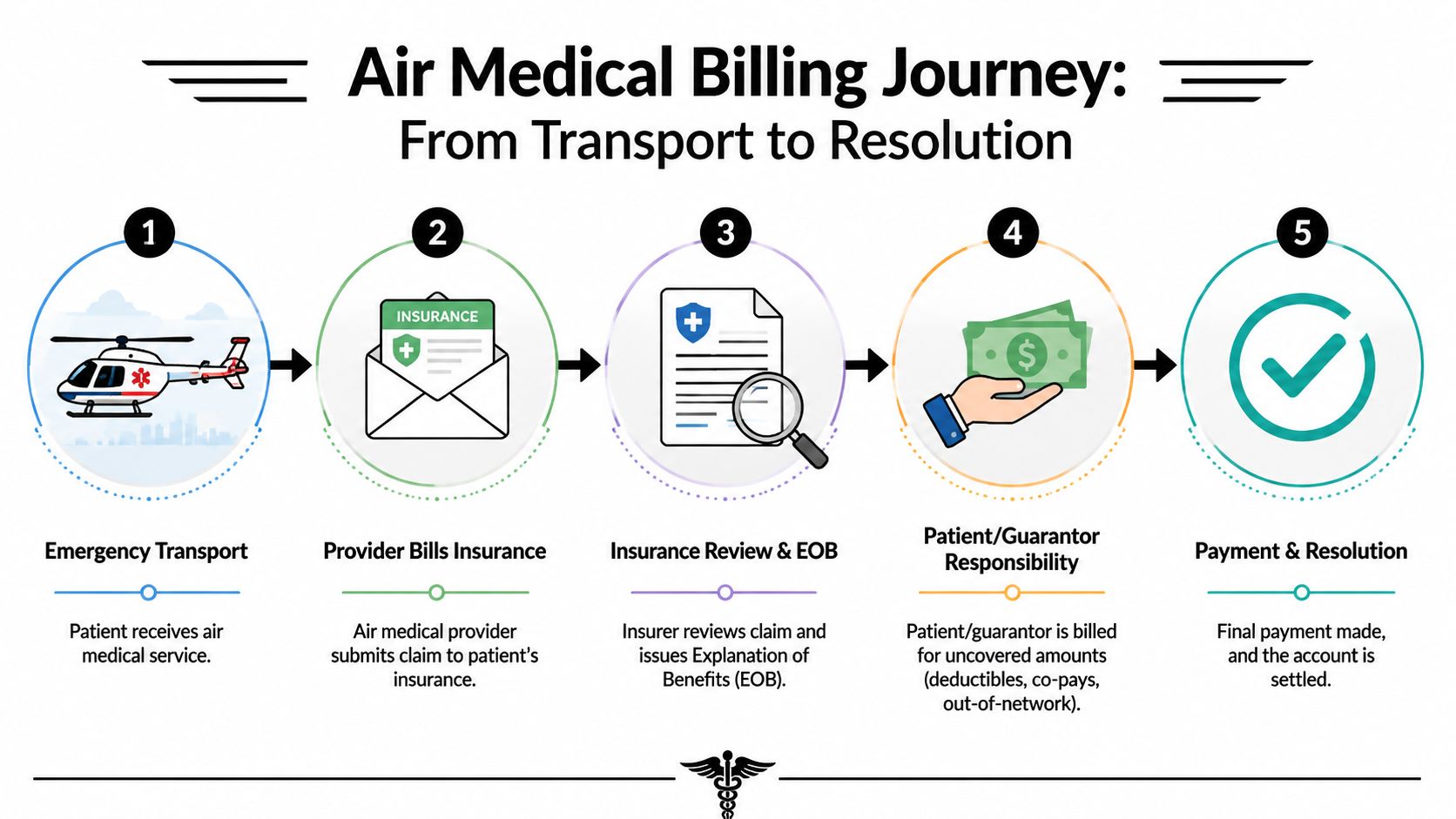

Insurance rarely moves in a straight line on air ambulance claims. The provider submits records. The insurer reviews them. The hospital may send supporting documentation. The family gets an explanation of benefits that doesn't always match the contract language they signed.

Why the payer mix gets messy

Air medical billing often involves what operators informally treat as payer triangulation. The family may sign the contract, the hospital may coordinate the transfer, and the insurer may decide what it will reimburse. Each one moves at a different pace and uses different standards.

That mismatch is one reason clean drafting matters. When contracts don't clearly define dispute handling, providers can see a 35% increase in administrative overhead and a 25% delay in collection. In plain language, unclear paperwork produces more calls, more appeals, and more waiting.

What the guarantor is really agreeing to

A guarantor isn't just the emergency contact. The guarantor is the person the provider can pursue if there's an unpaid balance after insurance processing. That's why the signature line matters.

Before signing, ask these direct questions:

If insurance denies the claim, what happens next

Ask whether the provider appeals first, bills the guarantor immediately, or does both in parallel.Will the provider bill insurance directly

In this context, assignment of benefits and claim cooperation clauses become important.What documents will the family receive

You should expect the transport agreement, any patient responsibility statement, and post-claim billing updates.

For families dealing with accident-related transport, broader injury billing issues can overlap with health coverage, auto coverage, and liability claims. A practical outside resource is this Philadelphia truck accident medical bill guide, which helps explain how medical bills can be routed and contested after a serious incident.

Insurance approval is not the same as contract protection

A family may hear that transport was medically necessary and still face coverage friction. A payer may also ask for records that weren't available at dispatch. For that reason, coordinators usually tell families to separate three questions:

| Question | Who answers it | Why it matters |

|---|---|---|

| Was the flight clinically appropriate? | Physician and transport team | Determines whether transport should occur |

| Will the insurer reimburse? | Insurer | Determines claim payment outcome |

| Who owes any remaining balance? | Contract and applicable law | Determines final liability path |

If you're reviewing public coverage questions, a plain-language explanation of whether Medicare covers air ambulance can help frame what insurance may and may not pay.

One practical example of a provider-side workflow is Med Jets by Air Trek, which verifies patient insurance information as part of transport coordination to help identify possible reimbursement routes before final out-of-pocket responsibility is known.

Your Rights Under the No Surprises Act

A family signs a flight agreement at the bedside, then gets a bill weeks later that looks far larger than expected. That is often the moment they learn the contract is only part of the financial picture.

The No Surprises Act can limit what a patient owes for many out-of-network air ambulance transports. If the flight is covered by the law and is not part of an All-Payer Model Agreement, patient cost-sharing is generally tied to the Qualifying Payment Amount (QPA), which is usually based on the median in-network rate, as explained in the CMS overview of key consumer protections. In plain terms, the provider's contract language does not automatically override federal billing protections.

This point gets missed often. A guarantor clause may say the signer is responsible for any unpaid balance. Under the No Surprises Act, that broad wording does not always control the final patient bill for an out-of-network air ambulance claim.

What QPA means in plain English

QPA works like a benchmark for calculating the patient's share on a covered out-of-network claim. It is not the provider's full billed charge. It is also not merely the largest number printed in the agreement.

That distinction matters in real cases. I have seen families assume that signing the contract meant they had agreed to any balance the insurer did not pay. The law can narrow that exposure. The dispute over the rest of the payment may continue between the insurer and the provider, while the patient's share stays tied to the legal cost-sharing rules.

If the agreement says you may owe the full unpaid amount, ask a second question right away. Does this transport qualify for No Surprises Act protection, and if so, how was the patient responsibility calculated?

Air ambulance claims are frequently contested on first pass, as noted earlier from CMS. An initial denial or partial payment does not automatically mean the full balance becomes the family's responsibility.

If a bill arrives, ask for clear answers to these points:

- Was the transport processed as an out-of-network air ambulance claim under the No Surprises Act

- What amount was used to calculate patient cost-sharing

- Was the QPA used

- Is this bill final, or is it a temporary balance while the claim or payment dispute is still under review

The practical takeaway is simple. Read the contract, but do not stop with the contract. For air ambulance bills, the No Surprises Act may give the patient protections that are stronger than the broadest payment language on the signature page.

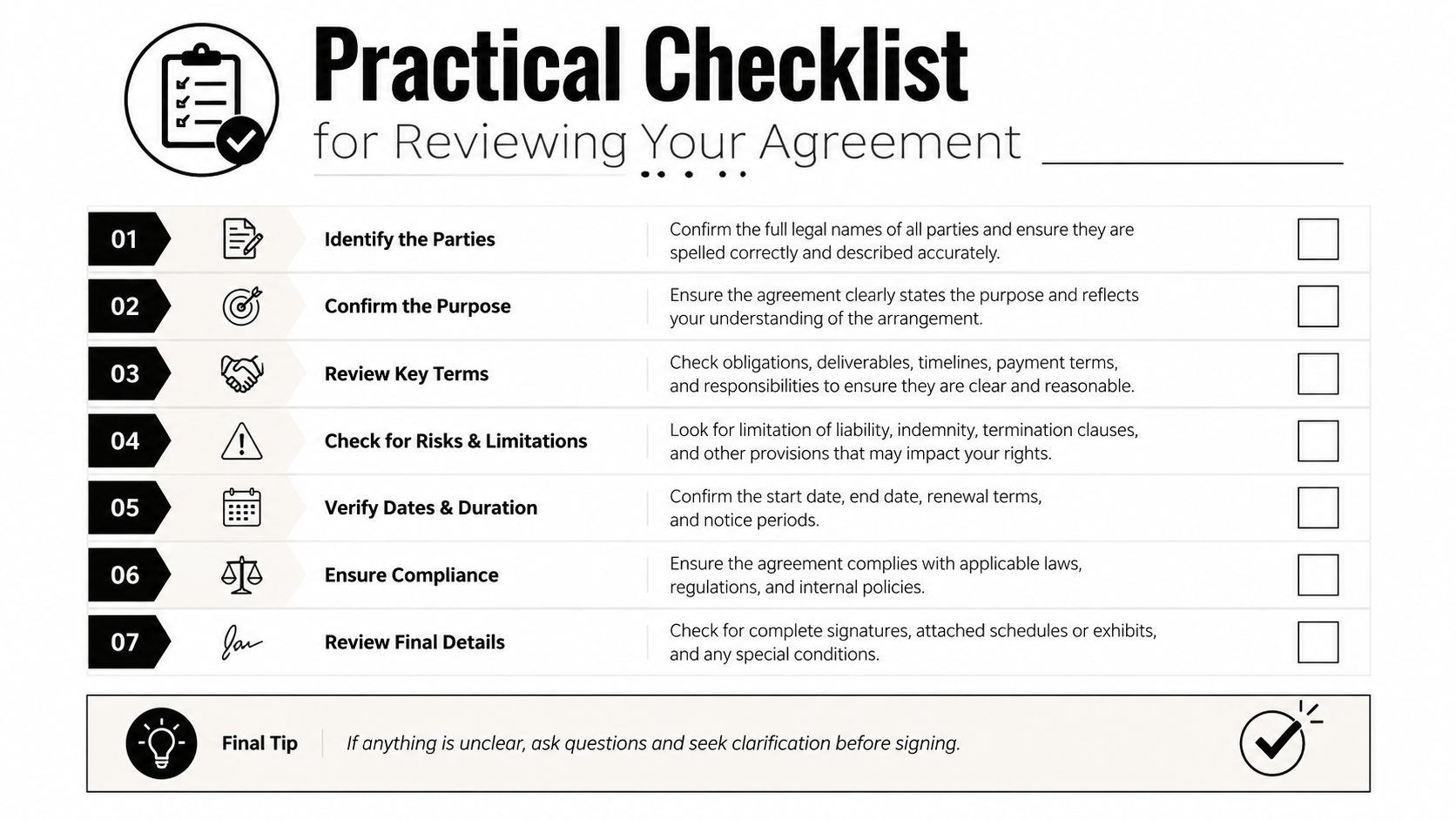

Practical Checklist for Reviewing Your Agreement

When you're on the phone with a coordinator, the best approach is simple and specific. Don't ask, “Is everything standard?” Ask questions that force a clear answer.

Questions to ask before signing

Who is the guarantor on this document

Make sure the financially responsible party is identified correctly.What payment is due now, if any

Ask whether the flight requires advance payment, partial deposit, or billing after service.What events change the price or refund amount

Focus on weather delays, medical instability, destination changes, and cancellation after crew activation.

Documents to request

A complete copy of the signed agreement

Not just the signature page.An itemized quote or fee summary

Even if final insurance payment is unknown, you want the service and billing framework in writing.Insurance submission details

Ask whether the provider will bill directly and what information they need from you.

Keep one working file with the contract, quote, hospital transfer notes, and insurer correspondence. Billing confusion grows when records are spread across phones, inboxes, and bedside paperwork.

Red flags worth slowing down for

Some contract terms deserve a pause, not because they're always wrong, but because they need explanation.

Broad liability language with no billing process details

If the agreement says you owe all unpaid amounts, ask how appeals, denials, and patient protections are handled.No cancellation language

A medical flight can change quickly. The contract should say what happens if it does.No dispute path

You need to know where to send a billing challenge and what happens while it's being reviewed.

A useful final question is, “If this claim is denied first, what exactly happens next?” The answer tells you a lot about how organized the billing process really is.

Frequently Asked Questions

Can payment terms and conditions be negotiated

Sometimes, yes. Payment terms vary across industries, and transportation businesses often work on 30 to 120 days, according to GoCardless guidance on average payment terms by industry. In practice, that means timing and structure aren't always fixed. A provider may not change the core rate, but may discuss deposit timing, accepted payment methods, or how post-claim balances are handled.

What if the flight is canceled because the patient becomes unstable

Ask for the written cancellation clause and refund policy. In air medical transport, medical or weather changes are not unusual. You want to know what counts as a refundable event, whether standby costs are retained, and how long billing review takes after cancellation.

Does signing as guarantor mean insurance won't be billed

No. It usually means you remain responsible if insurance does not fully resolve the account. The provider can still bill insurance directly if the agreement includes assignment of benefits.

Are payment plans available

Some providers offer them and some don't. The important part is to ask before signing, not after a balance ages. If the family has trouble with digital payment access or needs a different method, raise that early so the coordinator can say what options exist.

Can the contract override my rights under federal law

Not automatically. Contract language matters, but it does not erase applicable patient protections. If the bill involves out-of-network air ambulance charges, ask whether the No Surprises Act applies and how the patient share was calculated.

What's the most important sentence to get answered before I sign

Ask this: “After insurance processes the claim, how will you determine what I owe?”

If the coordinator can answer that clearly, the rest of the document usually becomes much easier to understand.

If you're reviewing an air ambulance agreement and want a clear explanation of the financial terms before transport moves forward, speak directly with the provider's billing or coordination team and ask for the clauses above in plain language, in writing.